by Jodie | Sep 18, 2017 | Budget, Budgeting, Debt Management, Finances, Savings, Wealth

Help your teens and young adults manage how they spend and save.

So your teenagers and young adults know how to spend, but do they know how to budget for the things they really want? Learning good money management should be an essential life skill.

A reason to save

For many teenagers and young adults with part-time jobs, spending their entire pay each week is easy if they don’t have pressing financial obligations. This is why it’s important to discuss a long-term goal and find a reason to save.

Perhaps this goal will be a car, a holiday with friends, higher education – or even a rental bond if they want to move out. Just make sure you emphasise that they will still need money after the purchase, either for running costs or to enjoy their social lives, so they shouldn’t blow the lot.

Budget benefits

The envelope method is a great way to learn about budgeting. Label real envelopes – or use tags in an app – with categories such as clothes, nights out, transport, phone, food, and university or school supplies. These should cover all their current expenses. Then allocate money to each envelope every pay day.

They can also use MoneySmart’s Budget Planner and apps such as TrackMySPEND to help them work out their goals and how much to allocate to each envelope.

A handy budgeting formula is the simple 50/30/20 rule. Urge them to dedicate 50 per cent of their pay to bills (if they don’t have many, they could reduce this amount), 30 per cent to fun activities and purchases, and 20 per cent to savings. This will get them into the habit of planning their spending and eliminate the habit of living from pay day to pay day.

Learning budgeting and savings skills early will help them build a solid nest egg for their future.

Get advice

Young adults face many big decisions, but helping them get serious about money management early can make life easier as they get older.

A visit to your financial adviser with your child may also help them develop good money management skills.

by Jodie | Aug 21, 2017 | Finances, Retirement, Superannuation

Many of the federal government’s superannuation reforms came into effect on 1 July. Here’s what’s new.

The government says it has tried to make the superannuation system more sustainable and has introduced more flexibility to suit modern work patterns. This is what has changed.

Additional 15 per cent tax for high income earners and concessional contributions cap

The income threshold at which high-income earners pay additional 15 per cent tax on certain concessional contributions has been lowered to $250,000 from $300,000. The annual cap on concessional (before-tax) contributions has also been lowered to $25,000.

The reduced threshold will affect about 1 per cent of account holders,[1] while the lower annual concessional contributions cap will affect about 3.5 per cent.[2]

Non-concessional contributions

The annual non-concessional contributions cap has been cut to $100,000 and $300,000 for those eligible to use the bring-forward provisions. Non-concessional contributions will no longer be available to people with total super balances of $1.6 million or more by the end of the previous financial year. People under the age of 65 will still be able to bring forward up to three years of non-concessional contributions.

This measure is expected to affect less than 1 per cent of fund members.[3]

Access to concessional contributions

Previously, only people who earned less than 10 per cent of their income from salary or wages could claim a tax deduction for personal superannuation contributions. Now, generally, anyone under the age of 65 – and those aged 65 to 74 who meet the work test – can claim a tax deduction up to the concessional contributions cap.

This will benefit the 800,000 or so people[4] who are partially self-employed and partially wage and salary earners, and individuals whose employers do not offer salary sacrifice arrangements.

The transfer balance cap

There is now a $1.6 million cap on the total amount that can be moved into the tax-free retirement phase. However, subsequent earnings on balances in the retirement phase will not be capped or restricted.

People with existing super income streams were required to take action by 30 June 2017 to ensure that they had no more than $1.6 million in super income streams. Additional time to comply is available for those who have a breach of $100,000 or less.

Less than 1 per cent of account holders[5] will be affected, as the average superannuation balance for a 60-year-old is expected to be $240,000 in 2017–18.

Low-income superannuation tax offset

A low-income superannuation tax offset replaces the low-income superannuation contribution. Under this measure, eligible individuals with an adjusted taxable income of up to $37,000 can get refunds on the tax paid on concessional contributions up to a cap of $500.

This avoids the situation where low-income earners pay more tax on contributions than on their take-home pay. The refunds will go into the superannuation account.

It is estimated that about 3.1 million low-income earners will benefit, including about 1.9 million women.[6]

Catch-up concessional contributions

People with a total superannuation balance of less than $500,000 before the start of a financial year can use any carried forward unused concessional contributions for up to five years. In 2019–20, this will help about 230,000 people.[7]

The spouse tax offset extended

The spouse tax offset is now available to more couples as eligibility has been extended to people whose recipient spouses earn up to $40,000. This is an increase from $13,800, and about 5,000 people are expected to use the change.[8]

Innovation barriers removed

The tax exemption on earnings in the retirement phase has been extended to encourage the creation of a wider range of products. This will provide more flexibility and choice for retirees to help them avoid outliving their savings.

Transition to retirement income streams

Taxable income from assets supporting transition to retirement income streams are no longer tax-exempt at the super fund level. Instead they will be taxed at 15 per cent.

Pension payments continue to be tax free if the individual is 60 or over.

Individuals will also no longer be allowed to treat certain superannuation income stream payments as lump sums for taxation purposes. About 110,000 people will be affected.[9]

Anti-detriment rule abolished

The anti-detriment provision that allows superannuation funds to claim a refund of the 15 per cent tax on contributions paid by the deceased member over their lifetime has been abolished. However, lump sum death benefits will continue to be tax-free.

Seek advice

As these changes are very complex, it’s a great idea to talk them through with an expert who may help you safeguard your financial future.

[1] Australian Government, The Department of the Treasury, ‘Superannuation Reforms’.

[2] Ibid.

[3] Ibid

[4] Ibid

[5] Ibid

[6] Ibid

[7] Ibid

[8] Ibid

[9] Ibid

![Fixed Income: Friend or Foe?]()

by Jodie | Aug 11, 2017 | General

Fixed income has been a friend to investors. Over the past 20 years, the annualised return to the end of last year for both domestic and global fixed income has exceeded global share returns. But with rates so low and bond prices so expensive, will fixed income become your foe?

Read on to find out why fixed income is in fact more relevant for your portfolio than ever before.

Diversification – Not all friends are the same

Traditional fixed income strategies play an important role in diversifying share market risk and cushioning portfolio returns during times of economic downturn. This is because fixed income returns generally have a low to negative relationship to shares. A negative relationship, or what is commonly referred to as a negative correlation, occurs when the value of one asset rises while the value of another falls. For example, in 2008 and 2011 Australian and global shares incurred large negative returns while fixed income funds posted strong positive returns.

Table 1: Australian and Global Equity returns verse Australian and Global Fixed Income returns in 2008 and 2011

| Year |

Australian shares |

Global shares |

Australian fixed income |

Global fixed income |

| 2008 |

-37.7% |

-28.4% |

11.2% |

3.6% |

| 2011 |

-11.1% |

-7.9% |

10.1% |

7.9% |

Source: Morningstar

Morningstar Categories: Australian Shares – Australia Equity Large Blend, Global Equities – World Equity Large Blend, Australian Fixed Income – Australia Fund Bonds – Australia, Global Fixed Income – Australia Fund Bonds – Global

The correlation between fixed income and shares can change over time and vary between different fixed income securities. Certain fixed income securities with higher credit risk, which is the risk that the issuer of the security will default, have historically become more correlated to shares when the share market is in freefall, while government bonds, with low credit risk, have generally remained a true diversifier.

Common Australian and global fixed income indices have a large proportion of their holdings weighted to government bonds. For example, the Bloomberg Barclay’s Global Aggregate index comprises of around 51% global government bonds. As traditional fixed income managers track these indices they will tend to hold a reasonable proportion of their portfolio in government bonds, and therefore continue to offer true diversification benefits.

Income – it’s nice to have friends that shout you

In addition to being a good diversifier, fixed income provides a positive, regular source of income returns. Income is provided by the coupon payments, which are essentially interest payments.

Currently, there are no investment-grade bonds (BBB or higher credit rating) that have been issued with a negative-rate coupon. So even if price returns for fixed income are negative, the income return via the coupon is currently positive. Even in Japan, where zero interest rate policies are in place, the coupon rate on investment-grade fixed income has remained positive.

Fixed income sceptics may point out that coupons are currently at very low levels. However, this is not to say opportunities don’t exist. Divergent interest rate cycles present opportunities for unconstrained bond funds.

Unconstrained bond funds are those managed without traditional indices or benchmark constraints. These strategies have the flexibility to ‘go anywhere’ and will invest across fixed income sectors, geographies and currencies. In practice this means unconstrained bond funds are able to tactically invest in countries where interest rates are rising and in emerging markets which offer higher yields. While this means taking on additional risk, there is the opportunity for higher returns.

Downside protection – Friends are there to protect

Fixed income is designed to help provide downside protection, meaning that steep losses should be more infrequent and limited in size compared to shares.

Historically, this has been the case and is illustrated by the below graph. The graph shows the global bond index, Bloomberg Barclays Global Aggregate index in dark blue, where the largest drawdown over 25 years was 4.9%[1] in 1994. This negative return is relatively small compared to Australian and global shares which have had maximum drawdowns of -47.2%[2] and -48.3%[3] respectively.

Graph 1: Drawdown of global fixed income verse global and Australian shares

Source: Lonsec Global Fixed Income – Bloomberg Barclays Global Agg TR (AUD hedged);

Australian Shares – S&P/ASX 200 TR Index AUD: Global Equiteis – MSCI World NR Index AUD

While negative returns for fixed income securities have been historically less severe when compared to shares, it is important to realise that just as friendships can have downturns, fixed income can also produce negative returns in certain periods of the investment and interest rate cycle.

For example, traditional fixed income strategies may struggle in a fast rising interest rate environment.

Nevertheless, certain unconstrained bond funds have absolute return targets and aim to achieve positive returns in all market conditions, including in rising interest rate environments. These style funds do not manage to an index and as a result typically have lower sensitivity to changes in interest rates.

Don’t break it off just yet

Those advocating a break-up are likely to tout that increasing interest rates are going to hurt fixed income funds, particularly the traditional variety. While in the short term there may be some pain, over the longer run a rising rate environment offers investors the opportunity to reinvest at higher interest rates (coupons), which is a positive.

Despite the US Federal Reserve hiking rates four times since December 2015, we have seen both Australian and Global Fixed Income return positive 2.5% and 2.7% over the last 12 months[4]

So when considered for the sum of all its parts, fixed income can offer great attributes to your portfolio. Whether it is traditional or unconstrained – each has different benefits to offer your portfolio making fixed income a true and long term friend.

Disclaimer: The information provided in this document, including any tax information, is general information only and does not constitute personal advice. It has been prepared without taking into account any of your individual objectives, financial situation or needs. Before acting on this information you should consider its appropriateness, having regard to your own objectives, financial situation and needs. You should read the relevant Product Disclosure Statements and seek personal advice from a qualified financial adviser. From time to time we may send you informative updates and details of the range of services we can provide. If you no longer want to receive this information please contact our office to opt out. Financial Services Partners Pty Ltd ABN 15 089 512 587, AFSL 237590

[1] BBgBarc Global Aggregate TR Hedged AUD Data from Morningstar between 1 Jan 1994 to 31 Dec 2016

[2] S&P/ASX 200 TR AUD from Morningstar between 1 Jan 1994 to 31 May 2017

[3] MSCI World NR AUD from Morningstar between 1 Jan 1994 to 31 May 2017

[4] Australian fixed income – Bloomberg Composite Bond All Maturities, International Fixed Income – Barclays Global Aggregate Bond Index (hedged) as at 31 May 2017

by Jodie | Jul 3, 2017 | Advisers, Australian Economy, Economy, Finances, Wealth

First-home buyers get some help

State and federal governments are creating new incentives to help first-home buyers get into the overheated housing market.

Buying your own home is the largest purchase decision most people will make in their lives.

However, a long run of low interest rates has fuelled spectacular dwelling price growth, record housing debt and phenomenal asset values, particularly in Sydney and Melbourne. According to the Reserve Bank of Australia, housing prices nationally have increased 7.25 per cent a year, on average, over the past 30 years.

Financial analysis and advisory firm CoreLogic adds that housing affordability has worsened over the past 15 years by every measure. It now takes 1.5 years of household income to save for a 20 per cent deposit on a dwelling compared with 0.8 years 15 years ago, the firm’s Perceptions of Housing Affordability Report 2017 shows.

Government assistance

There are incentives prospective first-home buyers can use to make their dream of owning their own home come true. This year’s Federal Budget, for example, proposes allowing individuals to make voluntary contributions to their superannuation accounts to save for a house deposit.

It is proposed that super contributions and earnings be taxed at 15 per cent, rather than higher marginal rates. Withdrawals would be taxed at their marginal rate, less 30 percentage points. Contributions would be limited to $30,000 per person in total and $15,000 per year and both members of a couple could take advantage of the scheme.

Additional non-concessional contributions could also be made but would not benefit from the tax concessions apart from the earnings being taxed at 15 per cent.

Currently, the NSW and Victorian governments offer first-home buyers:

• no stamp duty on all homes worth up to $650,000 in NSW and $600,000 in Victoria

• stamp duty relief for homes worth up to $800,000 in NSW and $750,000 in Victoria

• a $10,000 grant for builders of new homes worth up to $750,000 and purchasers of new homes worth up to $600,000 in NSW

• no duty on lenders mortgage insurance in NSW

• a $20,000 grant for new homes built in regional Victoria valued at up to $750,000 – which is double the amount available in metropolitan areas.

Most states also have first-home buyer grants, each with different criteria.

Some state governments are also making it harder for foreign investors by increasing duties and land taxes and introducing other measures to reduce competition for first-home buyers.

Seek advice

There are many investment options that can help you build a deposit, each of which has different risk and return factors, but you don’t have to make financial decisions by yourself. Talk to a Wealth Planning Partners Adviser to develop a plan that’s tailored to you. Your adviser can help you:

• understand your current situation

• identify your financial and savings (home deposit) goals

• determine your current income needs

• prepare a budget

• start a home savings plan

• protect your income and assets through personal insurance.

Sources: https://www.rba.gov.au/publications/bulletin/2015/sep/pdf/bu-0915-3.pdf https://www.corelogic.com.au/resources/pdf/reports/housing-affordability/2017-05-CoreLogicHousingAffordabilityReport_May2017.pdf?language_id=1 |

by Jodie | May 12, 2017 | Australian Economy, Finances, Taxation

Budget 2017 has proposed a few tax changes. Read about them here:

Medicare levy

- Rises from 2.0% to 2.5% from 1 July 2019 to help fund the National Disability Insurance Scheme.

Capital gains tax discount for investors in affordable housing

- Managed investment trusts will be allowed to develop and own affordable housing. Investors will get a capital gains tax discount of 60 per cent.

- Investors will get a capital gains tax discount of 60 per cent provided that they invest in qualifying affordable housing.

Small business accelerated depreciation extended

- Immediate deduction of assets up to $20,000 extended to 30 June 2018.

Education costs

- Eligibility for student payments will be limited to people undertaking courses approved for VET student loans.

- Existing student payment recipients will be grandfathered for the duration of their current course unless there is a break in their payment entitlement.

- You may wish to consider this if you want to fund your child’s education costs.

by Jodie | May 12, 2017 | Finances, Investments, Money, Wealth

The Government has announced some Incentives to improve housing options. Among these, are:

- Allowing first-home buyers to save a deposit through voluntary contributions to superannuation

- Disallowing travel deductions for investment residential property

- Limiting depreciation deductions for plant and equipment on residential investment properties

- Tightening the capital gains tax rules for foreign investors

- Reforming foreign investment rules to discourage investors from leaving properties vacant.

First-home buyers can use super

- First-home buyers will be able to use voluntary contributions to their existing superannuationfunds to save for a house deposit.

- Contributions and earnings will be taxed at 15 per cent, rather than marginal rates, and withdrawals will be taxed at their marginal rate, less 30 basis points. Contributions will be limited to $30,000 per person in total and $15,000 per year.

- Both members of a couple can take advantage of the scheme.

- Non-concessional contributions can also be made but will not benefit from the tax concessions apart from earnings being taxed at 15%.

First-home deposit salary sacrifice case study

Louise earns $60,000 a year and wants to buy her first home. She directs $10,000 of pre-tax income into her superannuation account using salary sacrifice, increasing her balance by $8,500 after the contributions tax has been paid by her fund. After three years, she is able to withdraw $27,380 of contributions and the deemed earnings.

After withdrawal tax, she has $25,760 she can use for her deposit. Louise has saved about $6,240 more for a deposit than if she had saved in a standard deposit account. Louise’s partner, Craig, makes the same income and salary sacrifices $10,000 over the same period. Together, after three years, they have $51,520 for their first home, $12,480 more than if they had saved in a standard deposit account. (Source: 2017 Budget papers)

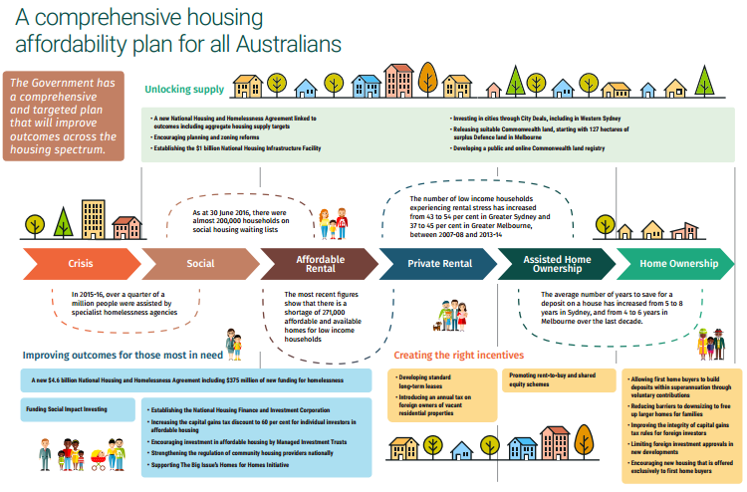

Unlocking supply

- The Government will help boost housing supply by:

- Providing $1 billion facility for critical infrastructure, such as water supplies

- Working with the States on planning and zoning reform to speed up development

- Releasing suitable Commonwealth land, starting with Defence land at Maribyrnong in Melbourne

- Investing more than $70 billion from 2013 to 2021 on transport infrastructure

- Specifying housing supply targets in new agreements with the States and Territories.

by Jodie | May 11, 2017 | Australian Economy, Centrelink, Finances, Money

Lots of Social Security changes have been proposed in Budget 2017. Here’s a highlights list of some of these. Please note that these are not yet enshrined in law.

Reinstating the Pensioner Concession Card

- This will be reinstated for pensioners who lost their pension following changes to the pension asset test on 1 January 2017.

- Those granted the Commonwealth Seniors Health Card (CSHC) as a result of the

- January changes will maintain entitlement to this card (and the energy supplement).

- The Low Income Health Care Card issued as a result of the January changes will be deactivated.

One-off energy assistance payment

- $75 for single and $125 per couple for qualifying pensions on 20 June 2017.

Family Tax Benefit Part A

- Changes to the income test for the Family Tax Benefit Part A payments may reduce entitlements. We need to identify and manage the impact of these changes.

Liquid assets waiting period

- The maximum waiting period for payments will increase from 13 weeks to 26 weeks and apply

where liquid assets are equal to or above $18,000 for singles (formerly $11,500) without

dependants or $36,000 (formerly $23,000) for couples and singles with dependants.

- It’s important to seek advice early (before termination) to see if we can lessen the impact of these changes. If you are affected, we need to manage cash flow during this period.

Newstart eligibility

Activity tests other than voluntary work may be required to receive Newstart allowances for people aged between 55 and 59.

Former Farm Household Allowance

Recipients who do not receive any other Commonwealth income support will be eligible for loans of up to 50% to refinance their debt to a maximum of $1 million.

Residency test changes

To be eligible for the Age Pension or Disability Support Pension, some claimants will need 15 years of continuous Australian residence (up from 10 years). Generally this won’t affect existing recipients.

Consolidation of payments

- Seven working-age payments and allowances, including NewStart, will be consolidated into one payment called a JobSeeker payment.

- Key elements include aligning the participation requirements for recipients aged 30 to 49 with those for recipients under 30, and recipients aged 55 to 59 will only be able to meet up to half of their participation requirements through volunteering.

- Recipients aged between 60 and Age Pension age will have a new activity requirement of 10 hours per fortnight that can be met through volunteering.

by Jodie | May 11, 2017 | Australian Economy, Budget, Money, Taxation

WINNERS!!

First home-buyers

First home-buyers can save for a deposit by salary sacrificing into their super.

Downsizers

Downsizers, 65+, can contribute up to $300,000 each to super from the sale the family home

regardless of satisfaction of the work test, total super balance or if aged 75 or over.

Investors

Negative gearing stays for mum and dad investors but travel claims for investment residential properties will be denied and capital expenditure eligibility will be tightened.

Schools

$18.6 billion has been earmarked for extra funding for schools over the next decade.

LOSERS!!

Taxpayers

The Medicare levy will increase to 2.5% to help fund the National Disability Insurance Scheme.

Tertiary students

University fees will rise by $2,000 to $3,600 for a four-year course and students will have to start paying back their debt when they earn more than $42,000 from July next year, down from $55,000. A 2.5 per cent efficiency dividend will be applied to universities for the next two years.

Child care changes

Only to families with incomes below $350,000 per annum (in 2017-18 terms) will get the child-care subsidy from 2 July 2018. The upper threshold will be indexed annually from 1 July 2018.

Banks

The five biggest banks will be charged a levy, raising $6.2 billion over four years.

Tax avoiders

The ATO will target tax avoidance by multinationals and big business.

by Jodie | May 11, 2017 | Advisers, Australian Economy, Budget, Finances, Retirement, Superannuation

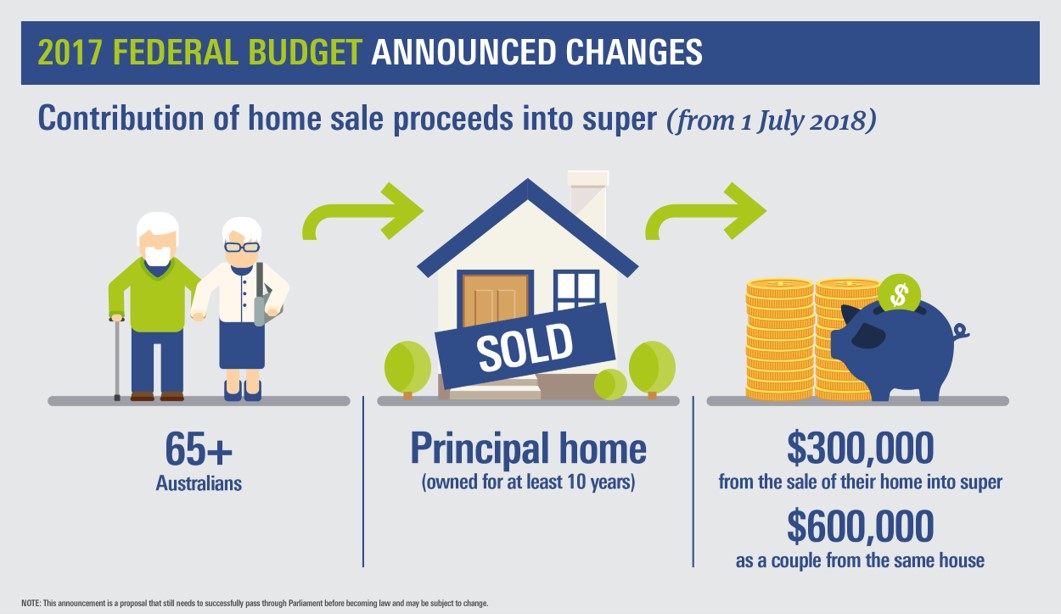

As you’re not doubt aware, the Federal Government announced it’s 2017 Budget this week and one of the surprise outcomes was the Downsizing Contribution for those looking to move out of a larger family home. Here’s a little more about how that works…

Downsizing contribution

People aged 65 or over will be able to make a non-concessional contribution to their superannuation of up to $300,000 each from the proceeds of selling their principal residence.

- Work test does not apply

- Residence must be held for a minimum of 10 years

- Total superannuation balance restrictions of $1,600,000 do not apply

- Restrictions eased on people aged 75 or over.

Downsizing contribution Case Study

John is 75 and Jane is 69 and they both have retirement income streams. They sell the home they have lived in for more than 10 years to downsize and the proceeds are $2,000,000.

George has room under the $1.6 million transfer balance cap. He can make a non-concessional contribution of $300,000 to superannuation and may choose to use the contributed proceeds to start a new account-based pension.

Jane has already used her transfer balance cap. She can make a non-concessional contribution of $300,000 to superannuation. As she has no room under her cap she cannot start a new pension with the contributed proceeds.

It’s worth having a chat with your Adviser to see if this is the best strategy for you, as you may lose Centrelink entitlements, depending on your new circumstances.

by Jodie | May 1, 2017 | Budget, Centrelink, Finances

The chances are you dutifully file your tax returns every year but are you making the most of your government entitlements? In this article,

we guide you through some key entitlements available for families.

Are you confused about your government entitlements? The good news is the recent overhaul of the Department of Human services no longer means lengthy waits in government office queues or listening to hold music while trying to organise your childcare rebate.

With automated payments and the user-friendly MyGov website, there has never been a better time to take a fresh look at your entitlements.

The birth of a child

Taking time out to care for a newborn can be expensive. However, since January 2011 primary carers now have access to government-funded parental leave payments, which are currently made for up to 18 weeks. There is also a 2-week payment available to eligible dads or partners assisting with a newborn.

Assistance with childcare

To encourage parents with young children to remain in the workforce, there are some great benefits on offer to working parents.

If you have children attending approved childcare and meet the income test (currently below $160,308 for families with two children), you may be entitled to the Child Care Benefit to help with the cost of daycare, vacation care or before and after-school care.

Higher income families may still claim the Child Care Rebate, which covers up to 50% of out “of pocket childcare expenses, up to an annual limit of $7,500.

Assistance for low to medium income families

Single parents and low to medium-income families can take advantage of a range of tax breaks and payments that can make raising a family more affordable. These include:

- The Single Income Family Supplement, which provides an annual payment of up to $300 to

help eligible households. The main income earner must earn between $68,000 and $150,000 and any secondary income earner below $18,000.

- The Parenting Payment for single parents with children under 8 or parents with partners with children under 6 who meet certain income tests.

- Family Tax Benefit for lower income families with dependent children under 20 (which includes grandparents assisting with childcare).

Summary

We have outlined just a few of the benefits that can help with the cost of raising a family.

To find out more about your entitlements, visit the Department of Human Services website.