by Amanda Cassar | Oct 7, 2020 | Australian Economy, Budget

Federal Budget Update 2020 is out. See how this may affect your family.

Proposals

The Federal Budget Update 2020 is out, and is all about jobs, and spending to make more jobs. We already have JobSeeker and JobKeeper, and now we have JobMaker and JobTrainer.

The announcements in this update are proposals unless stated otherwise. These proposals need to successfully pass through Parliament before becoming law and may be subject to change during this process.

Announcements…

Each announcement the Treasurer made was translated into jobs. Tax cuts for 11 million taxpayers equals 50,000 new jobs; expanding the instant asset write-off and the carry back of current losses is another 50,000 jobs. Bringing forward the Stage 2 personal income tax cuts were the order of the day, and there will be no increases in tax in order to pay for spending. So unlike other economic downturns, there will be no deficits tax on high income earners.

One key theme throughout the Budget, is that the Government is keen to improve outcomes for young people. We know this recession has hit young people hard and many have taken early release of their super.

For more information about how the Budget may affect your family, click here.

Or contact your Gold Coast advisers at Wealth Planning Partners to see if you’re impacted. Call your Financial Planners at Robina on 07 5593 0855 to discuss further.

by Amanda Cassar | Sep 28, 2020 | Advisers, Australian Economy, Budget, Budgeting, Finances, General, Retirement, Superannuation

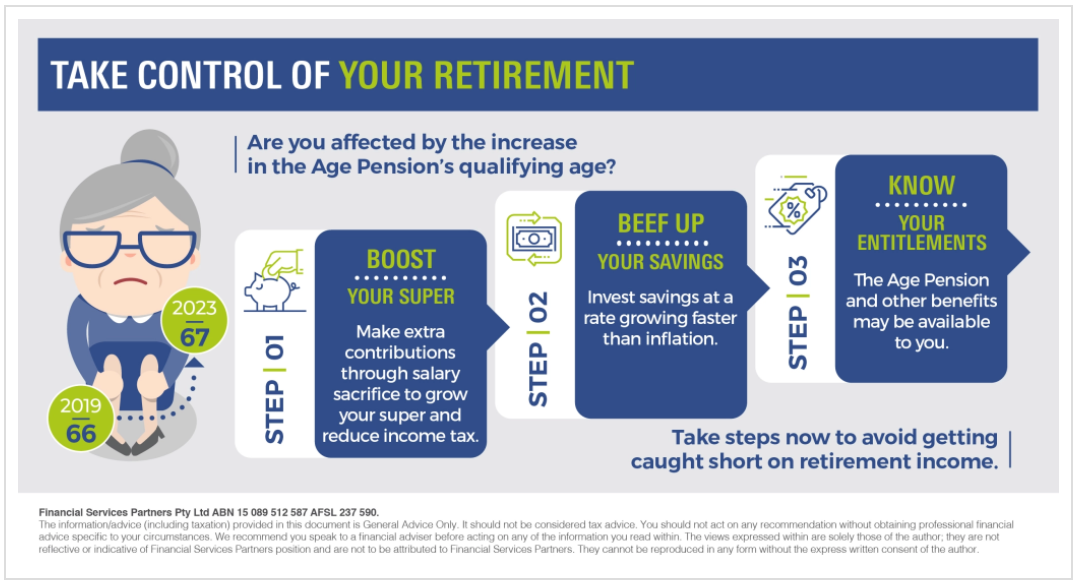

Are you affected by the increase in the Age Pension’s qualifying age? Take steps now to avoid getting caught short on retirement income.

The minimum age to qualify for the Age Pension has started going up. For those born on or after 1 July 1952, the qualifying age increases by six months every two years until it reaches 67 in July 2023. It rises to 66 in July this year.

So, if you’re turning 45 this year and plan to retire when you reach 60, you will need to wait until 67 before you can apply for the Age Pension. You’ll have to rely on your own savings and super. This makes it crucial to ensure you have enough money put away. But, the good news is that there’s still time to grow your retirement savings. So just how do you take control of your retirement savings?

Boost your super

Contributing more to your super can be a reliable route to bolstering your retirement fund. By making extra contributions through salary sacrifice, you can grow your super and at the same time reduce the amount of income tax you pay. The government will tax salary sacrificed contributions at 15 per cent. This could be much lower than your personal marginal tax rate.

Making non-concessional or after-tax contributions is another option. You can contribute up to $100,000 each financial year if your total superannuation balance is less than $1.6 million. To understand how these contributions work, it’s wise to get professional advice.

Jump onto the MoneySmart Superannuation Calculator to see how much you could have in retirement.

Beef up your savings

Your personal savings can supplement your super payments in retirement. But are they growing enough now to provide you with some income when you retire?

To build up your savings, you may have to invest part of it and make sure it’s growing faster than the rate of inflation. Investing in a managed fund or buying an investment bond may help you increase your nest egg. Seek professional advice to see if these instruments are appropriate for you.

Know your entitlements

Besides the Age Pension, you may be eligible for other government benefits and concessions. The Seniors Card, offers individuals over 60 discounts on some commercial and public services. Concessions that allow you to buy prescription medicine at a discount are also available.

But keep in mind that these benefits have strict eligibility rules. There’s also no guarantee that these entitlements will still be available by the time you retire. So take charge of your retirement today. By working with your financial adviser, you can develop a strategy that helps ensure you’ll be well provided for regardless of changes to pension policies.

If you’d like more information on how to take control of your retirement savings, reach out to the Team at Wealth Planning Partners.

by Amanda Cassar | Sep 28, 2020 | Advisers, Finances, Investments, Money, Savings, Self Managed Superannuation Funds, Superannuation

So, how do you invest your money? When deciding how to go about investing those hard earned dollars, you need to decide whether you’ll:

- do it yourself, or

- pay a financial advisor to do it for you

Both options have their pros and cons. However, you can – of course, do a bit of both.

Buy, sell or invest yourself

The advantage of choosing to invest yourself is that you’re in control of all the decisions. It will also save you money by making it cheaper than paying a financial advisor to invest your money. The down-side risk is that you may overrate your expertise and may not diversify.

If you choose to invest directly, it’s important to have a thorough plan and put in the time to research your investments. You should also keep track of how they’re performing.

Use a professional investment manager

If you decide to invest in a managed fund, some managed accounts, exchange-traded fund (ETF) or a listed investment company (LIC) your money is pooled with other investors. A professional investment manager then buys and sells investments on your behalf.

When using a professional, you benefit from their skills and expertise to make investment decisions. However, have to pay fees for this service. These can include management fees, administration fees and entry and exit fees.

See managed funds and ETFs to learn more about these investments.

Investing with a financial adviser

Seeking a financial adviser can assist you further by setting your financial goals, understand your risk tolerance and find the right investments that are suitable to you and your circumstances.

Make sure your financial adviser has an Australian financial services (AFS) licence or is an authorised representative. Check their qualifications on the Financial Advisers Register.

- Decide what it is that you want from the advice. Would you like help with investing money, budgeting or planning for retirement?

- Ensure that you read your adviser’s Financial Services Guide (FSG) to learn about their fees and services, and how they deal with complaints.

- Do your due diligence by comparing the fees charged by different advisers, to make sure you’re getting a good deal.

- Be careful about how much access your adviser has to your investment accounts.

Ensure that you talk to your adviser if you have any questions with regards to their advice and ensure that you understand their explanations in full.

If you’d like the Team at Wealth Planning Partners to assist, we’d be more than happy to help. Just reach out on 07 5593 0855.

by Amanda Cassar | Sep 21, 2020 | Advisers, Budgeting, Economy, Finances, Financial Stress, Investments, Retirement, Savings, Superannuation

Is it time to consider your retirement lifestyle needs?

Considering the cost of living and your expected annual retirement income, is crucial to retirement planning.

So, how do you consider your retirement needs? For the record number of Australians transitioning into retirement, the increasing cost of housing is a hindrance. Many are struggling to pay off their property before they retire, and this may lead to a few common scenarios:

- Being forced to sell the family home prior to retirement and renting or downsizing

- Continuing to pay down the mortgage on the home they live in, but leave beneficiaries with an asset that has debt owing

- Long-term renting due to lack of affordable properties on the market

- Short-term renting in different locations as a way of chasing the nomadic lifestyle dream without the financial burden of a mortgage.

And. deciding where and how you want to live can be fraught with stress. This can occur whether you’re about to retire or you’re if you’re watching your parents prepare for retirement. A recent survey by National Seniors Australia outlined that many people worry they will run out of savings and investments in retirement. Women worry more about retirement savings than men. Worrying is 65% higher in people who have less than $500,000 in savings. And at least 53% higher in people who expect their main source of income in retirement to be the Age Pension.[1]

How much money do you need to retire comfortably in Australia?

According to the Association of Superannuation Funds of Australia (ASFA), there are two broad categories of lifestyles in retirement — comfortable or modest. A comfortable retirement affords people a good car, private health insurance, dining out regularly, travel, and factors enjoyed whilst working. In a modest retirement, you may be entitled to the Age Pension, but you can only afford the basics, with occasional small luxuries.

How much do you need to live on?

There are facts and figures from industry bodies and experts, but your retirement lifestyle is unique to you. Mapping your retirement plan with a financial adviser can give you a clearer picture on what you can afford. As a benchmark, here are some widely touted figures:

- A couple of about 65 years of age – $40,194pa is needed to live modestly.

- A couple of about 65 years of age – $61,786pa is needed to live comfortably.

- For singles of about 65 years of age – $27,913pa is needed to live modestly.

- For singles of about 65 years of age – $43,787pa I needed to live comfortably.[2]

Can renting affect retirement income?

While these numbers help you understand cost of living in retirement, things become complicated if you don’t own your home. ASFA’s calculations are based on the assumption retirees will own their home before retiring. So, you don’t need need to allocate money towards mortgage or rent in the budget.

However, the Australian Bureau of Statistics (ABS) report that around 285,000 Australian households ren in retirement. While renting may afford the ability to live in a more desirable location, the cost still needs to be factored in. Therefore, the numbers provided by ASFA need to be tweaked if you are renting in retirement. And, this can blow out the figures of exactly what annual income you need to have access to.

Can you rent and afford a comfortable retirement?

Based on the ASFA’s calculations, if you retire in Sydney you would need $1,166,000 as a couple or $1,045,000 as a single. This is to afford a comfortable retirement lifestyle whilst renting. While the number may be lower for other cities and regional centres, it provides a more realistic calculation. Time to reassess exactly how much your retirement nest egg should be if you’ll be renting in retirement? Having a greater understanding of how you can structure your super funds can help you be better prepared.

As with other passive investments, ensure you’re not drawing down so much capital that your balance isn’t compounding. You need an adequate rate to provide you with enough retirement income for the rest of your life.

For example, if the average return on your super balance is 9% per year, it’s wise to drawdown 4% or less so you can maintain adequate funds. Retirement may be longer than you think? A good financial adviser can work through the calculations based on your individual circumstances, factoring home ownership or rent and any Centrelink benefits. Have you considered the retirement lifestyle you want without running out of money?

What if you don’t want to rent in retirement?

If you don’t own a home and you’re not keen on renting, there are other options. Maybe you want the freedom of living in a motor home, setting up in a modern tiny home, basing yourself in a retirement village, securing granny flat rights, or, living on a cruise ship. While these options may not be for everyone, the very nature of retirement, can give you the flexibility to live a nomadic lifestyle with a smaller carbon footprint. If you’re interested in staying in one place, a retirement village or granny flat can provide you with that lifestyle.

There is no one size fits all in retirement

When it comes to your retirement dreams and finances, your picture looks different to the next person. So, have you considered your retirement needs? If you don’t own your home, you’ll need to factor the cost of rent into your retirement planning. Be sure to ensure your nest egg and the annual income you’ll draw is enough to provide your desired retirement lifestyle. If you do own your home you won’t have to worry about the mortgage or rent. But, what about home improvements and modifications as you age?

With so many different scenarios to consider, it is wise to work through your options with your financial adviser. Reach out to the Gold Coast team of Financial Planners at Wealth Planning Partners if you’d like to discuss your individual needs.

by Amanda Cassar | Sep 21, 2020 | Advisers, Finances, Investments, Money, Savings, Superannuation

Do you know how to protect yourself against scams?

The onset of COVID has propelled social media and marketing to an all-time necessity and has resulted in increased predatory scams and virtual hacking, putting people at risk more than ever before.

Here are some suggestions…

Check to see if your email is legit by having a few checklist items that you go through. This can protect you against online scams and include:

- Avoid clicking on hyperlinks in text messages or social media posts, even if they appear to come from a trusted source.

- Never respond to any unsolicited messages or phone calls where they request personal or financial details. Press delete or hang up, no need to be polite. Scammers prey on people who are too nice to say ‘no’.

- Never provide a stranger remote access to your computer, even if they claim to be from a company such as Telstra or the NBN.

- Don’t be afraid to tell them that now isn’t a good time to talk. Do your due diligence. Go away to verify the legitimacy of a contact. Research them through an independent source such as a phone book, past bill or online search. Most companies will log the call in their computer system. So, when you ring them to verify their legitimacy, they should be able to check their records and see if anyone has called you.

- Keep personal devices and details secure by having a pin code to access and using strong passwords.

- Keep devices and computers up-to-date, with appropriate anti-virus software.

- Review your privacy and security settings on social media for both your personal and business pages.

- Use Two Factor Authentication wherever it is offered.

If you recognise suspicious behaviour, click on spam or have been scammed online, take steps to secure your account and be sure to report it.

Beware of superannuation scams

The early access to superannuation that the Government offered due to COVID opened new opportunities for deception and scams. People are attempting to steal Superannuation by offering unnecessary services whilst charging a fee. These schemes are illegal and heavy penaliies apply.

Most of these scams start by receiving an unexpected call claiming to be from a superannuation company or financial services firm.

- Never provide information about your superannuation to someone who has contacted you. This includes offers to help you access your superannuation early under the government’s new arrangements.

- Ask for the callers contact details, hang-up and then call the relevant organisation directly. Search for their details through an independent source such as a past bill or online search.

- Phone back and confirm with the agent that answers the call that they did call you with a genuine offer for assistance.

- For more information on superannuation scams visit ASIC’s MoneySmart website.

Once your checklists have been completed, be sure to share it with your family or the staff in your office. Place it somewhere visible in your home or office as a constant reminder.

If you’d like a second opinion on whether something is legitimate or a scam, reach out to your Wealth Planning Partners advisers at Robina.

by Amanda Cassar | Sep 14, 2020 | Advisers, Business, Finances, General, Money, Wealth, Women

The ongoing COVID situation means changes to how we do business.

If you are not able to visit us in person, or it is more convenient to work with us digitally, we have the capability and technology to make it easier for us to connect with you. Is it time to discuss your financial goals online?

We have also considered how we can do this in a safer online environment.

We want to make working with us as easy and convenient as possible. This is why we use technology to streamline the way we share information. With cyber attacks at an all-time high, we’re also taking steps to make sure we keep your personal information safe. You can share information with us without worrying it’ll end up in the wrong hands.

Digital Changes

Here’s what you can expect from us:

- a secure network and up-to-date devices

- regular back-up of our data

- no shared accounts or passwords

- a strong password management framework and two-factor authentication

- password protected documents if we need to share your personal information

- a process to report and resolve any suspicious activities or issues.

What can you do to further protect your personal information?

- install anti-virus software on all your devices and regularly update the software

- use a strong password or unique passphrase and activate two-factor authentication where possible

- don’t share your personal information or whereabouts on social media

- never give out your personal information over the phone unless you’ve properly identified the caller

- and let us know if you see an email from us that you think may be a scam.

Protecting your personal information will always be a priority for us, and we will continue to make it easier, and safer, for you to work with us. We’d be happy to discuss your financial goals online if this is your preference. And hey, there’s no parking or traffic issues either.

If you are ready to connect with us online, we would love to hear from you, so please get in touch. Learn more about the Gold Coast based Wealth Planning Partners team here.

Links to book with your preferred Financial Advisor for an online Zoom appointment are as follows:

Amanda Cassar

Principal Financial Advisor

15 min appointment

60 min appointment

Mitch Cassar

Financial Advisor

15 min appointment

60 min appointment

Alternatively, please do not hesitate to contact one of our friendly staff directly on 07 5593 0855.

by Amanda Cassar | Aug 31, 2020 | Advisers, Budget, Budgeting, Debt Management, Finances, Financial Stress, Money, Savings, Wealth

Learn how to manage your Financial Stress

As a Financial Advisor, we often have clients come to see us without their spouses, for investment or financial planning session. But then, there’s also many that never visit without their other half.

So, having problems getting out of debt is our number one challenge with couples, and unfortunately has a severe impact their relationship. And, it’s not easy to experience the emotional turmoil that financial duress can have. Perhaps fights about money have become so regular that marriage is hanging by a thread and may not stand the test of time.

Key Takeaways

- Research shows that more than half of marriages start off with a burden of debt.

- Making use of a Budget Planner, recognising and practising discretional spending, and boosting income are typical ways that a couple can reduce, and in some cases, eliminate debt and regain their financial control.

- In addition, couples can stop having arguments about finances by scheduling a weekly money “date” to discuss finances and sharing their family financial histories and experiences in a safe environment without judgement.

- Exercise compassion and patience toward your partner to reverse any negative historical experiences. This will enable positive emotions and thought patterns when having a conversation about your financial concerns.

Hidden Spending and

Ok so we’ve all done it… don’t lie! Hidden spending habits, which are so justifiable in one’s own mindset. We all tell ourselves “it was on sale. So, I’m practically saving money!”. Or the common fib used by some are “oh this old thing? It’s been in my wardrobe for ages!” Meanwhile, your partner is probably questioning their own sanity thinking their memory is playing tricks. Or, they know you’re lying and are less than impressed.

It’s paramount to have aligned goals with your partner when it comes to getting out of debt and increasing savings. Make it a goal to take the emotion out of money. Do you feel better when you have purchased something for yourself? It is giving oneself a good ‘pat on the back’ for working so hard. We are bombarded with marketing everywhere we turn. Billboards and advertising constantly play on our emotions. They tell us subliminally “if you buy this product, you will feel better about yourself.” Or “this will give people a better perception of how successful you are”.

It’s paramount to have aligned goals with your partner when it comes to getting out of debt and increasing savings. Make it a goal to take the emotion out of money. Do you feel better when you have purchased something for yourself? It is giving oneself a good ‘pat on the back’ for working so hard. We are bombarded with marketing everywhere we turn. Billboards and advertising constantly play on our emotions. They tell us subliminally “if you buy this product, you will feel better about yourself.” Or “this will give people a better perception of how successful you are”.

Today, people seem to value being recognised as being ‘successful’ or to be known as someone who is important, or of value. Individuals may feel that if they drive a certain car or can afford designer labels they will gain more respect by others. There is nothing wrong with having such material possessions or the creature comforts in life, however, there needs to be a healthy balance. It is easy to be trapped into living beyond ones means.

Unaligned Values or Goals

Sometimes we come across instances where one party in the relationship might spend more freely than the other, this can be met with frustration and irritation by the other spouse. It’s like watching a pressure-cooker on the verge of exploding… they reach a breaking-point and the emotional cracks rise to the surface to cause an eruption of some kind. Hurtful things can be said, which cannot be unheard, and it just snowballs from there.

If this sounds all too familiar, please know that you are not alone. According to a 2018 Fidelity study, more than half of couples getting married start off in the red. Even worse, 40% of indebted couples admitted it had a negative impact on their relationship.

Gold Coast based Financial Adviser Amanda Cassar of Wealth Planning Partners states: “Being a Financial Advisor, I have seen and experienced first-hand the negative tension that debt can have on a relationship. After spending time with clients, it’s clear to see that most couples want to save their relationship. That’s where we come in – We take the first step to initiate a tailored financial / investment plan to assist and alleviate their financial burden resulting in healthier financial life.”

Minimising Spending and Cutting Bad Habits

Speak with your partner and Financial Advisor about putting together a financial or investment plan. Set-up a clear budget that pinpoints where you can cut back on spending. Eliminate things like subscriptions and frequent dinners or takeaway. Cut back on bought lunches at work and the good old coffee habit. It also pays to take advantage of free facilities. Instead of joining a gym, make use of the free gym equipment down at the beach. Go for walks. Hey, even ride your bike to work if you are able to. Then you save on petrol too! Some measures may only be for the short time.

Create a Family Budget Together

Also, establish a grocery budget, and redirect any surplus into another account to be put towards debt repayments. Sometimes lowering spending isn’t enough. An increase in income may be required. If you’re a business owner, you might need to take on an extra client or two to give you that extra boost in income. Perhaps even a second job could help. Sell of unused items or monetise your side hustle.

And, set up a direct payment through your bank account to automate bill payments. It helps to know that your credit card and other payments are on a consistent scheduled date, that way you can just focus on making sure that the money is in your account ready at the time. It may be easier to break up payments into your pay cycle rather than waiting for monthly or quarterly invoices.

The Winning Factor!

The real breakthrough and victory for most couples is the fact that they start communicating more about their spending, savings goals, aspirations, and commenced planning for their financial future. Money goes from being a subject they fought about, to one they enjoyed spending time discussing without shame or blame.

To get to this point I highly recommend taking the time out to implement the following four simple rules:

-

Schedule weekly money dates

Weekly money dates will allow you and your partner to come into the conversation prepared, unthreatened, and ready to make progress. If these talks happen regularly, they won’t be left until something has gone completely wrong and off-track. Tempers and arguments are less-likely to get out-of-hand and are discussed more calmly and encourage growth and respect.

-

Share previous experiences about your family financial history with your partner

Don’t hide your previous experiences from your partner when it comes to your financial history. Learning how respective families talked about money and how these influences impact your current relationship. If one partner thinks it’s a taboo topic and normal to keep their spending secret, while the other wants expenses out in the open, there are bound to be expensive and painful miscommunications yet to be had. Go into the conversation with an open mind, find out what’s normal and what’s not in your partner’s eyes. What you thought was a bad-natured or deceitful act may have been a seemingly “normal” money habit to them, or vice versa.

-

Try to be more compassionate and exercise patience

Money issues are a bit of a touchy and sensitive subject and can impede on some peoples privacy whilst raising some deeply entrenched emotions to the forefront. By empathising with one another and allowing permission to admit past mistakes free of shame, this will welcome and encourage planning for the future. Remember that when dealing with personal finance, these issues touch more than a balance sheet. Pride, shame, and self-worth can easily be tangled up in discussions about money, so tread carefully and respectfully.

-

Create positive associations

So, by talking openly about financial aspirations and goals, you might find that a lot of fun was missing in your relationship when money was a source of stress. Once a plan is in place and clients see a viable path with managing their money, they actually enjoy their financial chats, since they now represented the positive possibilities awaiting them in the future, rather than feeling guilty and ashamed for not being where they want to be financially.

Time to manage financial stress

Also, it is extremely rewarding when you can see progress you make. This doesn’t mean every couple will have the same experience. But, they will have a better chance if they make the effort to start. Address conversations about money from an honest, open, and loving place. It takes sacrifice, commitment, checking your pride when necessary. Have a determination to follow a structured process to give you the best chance of success…

And, I’ve seen it happen, that’s why we are here! Reach out to the Gold Coast financial planning team at Wealth Planning Partners to chat further about your situation. We’d be happy to be an impartial third party in your money chats.

by Amanda Cassar | Aug 25, 2020 | Budget, Budgeting, Debt Management, Finances, Money, Savings, Wealth

Taking care of household finances can be taxing, especially if you have a big family. But with proper planning and budgeting, there’s no need to stress. Here’s five financial tips for large families. Learn to more effectively manage your household finances.

Here’s Five Financial Tips for Large Families

1 | Examine your finances

Sitting down as a family and figuring out how much money is coming in and going out may help you gauge the state of your family’s finances. A clear picture of your household income and expenses will set you up to manage cashflow better.

2 | Rein in spending

Keeping expenses under control can be tough in a large household. But if you’re spending as much as or more than you’re earning, you might want to consider limiting your family’s discretionary costs by buying only what you can afford. Cutting back and living frugally can help you stay on track.

3 | Set financial goals

Setting financial goals as a family may help you work towards future aspirations instead of simply meeting current expenses. Whether it’s buying a bigger house or going on a dream holiday, having a financial goal may help your family set priorities and stay on track financially.

4 | Keep a budget

Keeping track of spending may help you to better manage your family’s finances. By working with a professional financial adviser or money coach, you could create a budget that factors in not only income and expenses, but also financial obligations. Make use of the MoneySmart Budget Planner if you need somewhere to start.

5 | Build up emergency and retirement funds

Unplanned expenses such as unforeseen medical bills can put a dent in family finances. By growing your emergency fund to cover six months’ worth of expenses, you may be better positioned to handle unexpected events.

While it’s easy to neglect your own financial future when providing for your family, saving for retirement should not take second place. Keep in mind that the earlier you start saving, the better chance you have to grow a sufficient nest egg.

Working with an adviser

Managing finances for a big family need not be a painful exercise. By working alongside a financial adviser to keep track of your spending, and discussing money matters openly, you can succeed. Set financial goals as a family to make handling household finances is a task you can achieve together Make sure you implement these five financial tips for large families.

Or, contact the team at Wealth Planning Partners on 07 5593 0855 to find out if we can assist your family with their household’s financial needs.

https://youtu.be/uo7OzDLGdKc

by Amanda Cassar | Aug 17, 2020 | Advisers, Budget, Budgeting, Money, Savings, Superannuation, Wealth

Getting ahead in your 40’s?

Here’s 5 tips you need to consider to getting ahead in your 40’s..

Being in your 40s requires balancing many responsibilities and it can become easy to neglect your own financial wellbeing. However, it’s not too late to secure your future. By now you might have kids, a substantial amount of debt, career responsibilities and new and old relationships to navigate. Here are 5 tips to financially getting ahead in your 40s.

1 | Create a financial plan

If you don’t have a plan, it’s time to get one. Ensure that it’s based on your needs and priorities. By working with a professional adviser, you will be more successful to tailor a plan that helps you optimise your ability to save and invest.

2 | Grow your savings

Your 40s could be your peak earning years, so it may be a good idea to increase your savings and set aside a portion of your income into your superannuation or investment accounts. However, be sure to do your homework and consult with a professional financial adviser about your options.

3 | Give your super a “health check”

A quick super health check may help you optimise your retirement savings. For example, by choosing an alternative investment option or type of risk, you may be able to earn better returns on your super. If you have multiple funds, consolidating your accounts may help you save on fees. Again, it is wise to seek advice from a professional adviser before acting.

4 | Avoid lifestyle creep

People generally have a tendency to increase their standard of living as they earn more as they can afford more things, such as a better car or house. While it’s only natural to want the finer things in life, you’ll likely end up with little to no financial gain if your spending rises as quickly as your income. Try being disciplined and be aligned to your long-term financial goals and remember the big picture.

5 | Consider investing more

Your 40s may be a good time to invest more – or, diversify your investments – to help you grow your long-term savings. But keep in mind that it’s important to choose instruments that suit your risk appetite and time horizon. Developing a strategy with your financial adviser might make it easier to achieve the return required to reach your financial goals.

Getting ahead in your 40’s

Getting ahead on your own can be a bit daunting. Consider working with a financial adviser if you need assistance to reach our goals. These five tips can help you reach your financial goals. It’s good to start early.

Visit the MoneySmart website if you’d like to find out more about where to start.

Or, if you’d like the assistance of a financial adviser, reach out to the team at Wealth Planning Partners. We’ve helped many to achieve their financial goals. We’re Gold Coast based, but look after clients both via Zoom and in person. Contact us on 07 5593 0855 to find out more.

by Amanda Cassar | Aug 10, 2020 | Superannuation

“Early withdrawal of super” may leave youth $100k worse-off in retirement

Federal Opposition steps up attacks on coronavirus support measures. This allows people in hardship to withdrawal some super early.

Labour said the Covid-19 economic crisis will greatly affect the younger generation. It estimates someone aged 25 who withdraws $20,000 may be up to $100,000 worse off in retirement.

Early Access to Super Scheme

The opposition is stepping up attacks on government’s handling of early access to superannuation scheme. This enables those dealing with economic effects of Covid-19 to withdraw up to $10,000. And, people were able to access up to $10,000 last financial year.

Shadow assistant treasurer, Stephen Jones, states “young Australians have borne the brunt of this crisis and will be forced to continue to pay the cost in years to come”.

Australia is easing superannuation access for those worst-hit by coronavirus. But can we afford it? Read more

“After accounting for inflation and cost of living, a 25-year-old who withdraws $20,000 will be $80,000 to $100,0000 worse off in retirement. A 35-year-old who withdraws $20,000 will be around $65,000 worse off. Collectively, under 35s will be at least $51 billion worse off at retirement.” Jones.

However, the Labor party released estimates a few days after it asked the auditor general to look into failures in implementation of the scheme.

Early Super Scheme Releases to date

The superannuation early release program has currently paid out $32bn from retirement savings. This is is set to top $42 billion by December. Former PM, Paul Keating raised concerns 590,000 accounts had been withdrawn to a zero balance.

While Opposition says it supports the original intent of the scheme, it argues there has been insufficient checks. This is especially true on whether people accessing superannuation are in real hardship. Retirement savings have been exposed to fraudulent scams.

“They’re going to look back on this and think of this superannuation policy as being as dumb as the introduction of cane toads in Australia.” Jones told reporters, “this is a bad policy that has been poorly implemented.”

Fraud & Identity Theft

Allegations of identity theft involving 150 Australians prompted Government to temporarily halt withdrawals in May. Police froze $120,000, believed to have been ripped-off from retirement savings.

An interview with Guardian Australia and Assistant Minister for Superannuation, Jane Hume, said people had always been able to access their superannuation. This is especially true in times of financial distress. Hume accused Keating of being out of touch with needs of those who have early access to super.

“[It’s] extraordinary that a man in a Zegna suit on a generous parliamentary pension can sneer at the decisions made by ordinary Australians who are facing some of the most challenging economic circumstances we’ve ever seen,” Hume said.

And, Labour’s figures were based on the party’s own internal modelling.

Some calculations are broadly similar to estimates published by the Grattan Institute in the past last week. The thinktank argued much of the losses to such individuals would be offset by larger government-funded pension payments.

Long Term Outcomes

The Grattan Institute calculated a 35-year-old who took out $20,000 allowed under early release of superannuation would see total funds fall by about $80,000. Also, the institute indicated a person’s total retirement income would fall by only $24,000 in today’s dollars.

Brendan Coates, Grattan Institute’s household finances program director, said government’s priority when launching the scheme was to get money out quickly. However, he said it made sense to tighten checking of applications to ensure people were genuinely eligible.

And, Coates reaffirmed Grattan’s position the amount of compulsory superannuation paid should not increase, because of potential effects on wages.

Superannuation Contribution Increases

Hume told Guardian Australia scheduled increases in compulsory superannuation from 9.5% to 12% were already legislated. It would be “very difficult to unwind”.

Government has “no plan” to abandon superannuation guarantee increases. However, it would be “irresponsible” not to consider trade-offs between superannuation increases and wages.

Therefore, the government is considering a retirement incomes review. This was submitted to the prime minister and treasurer in late July.

If you’d like to discuss whether the withdrawal is right for you, please contact the team at Wealth Planning Partners to assess your situation.