by Jodie | May 11, 2017 | Advisers, Australian Economy, Budget, Finances, Retirement, Superannuation

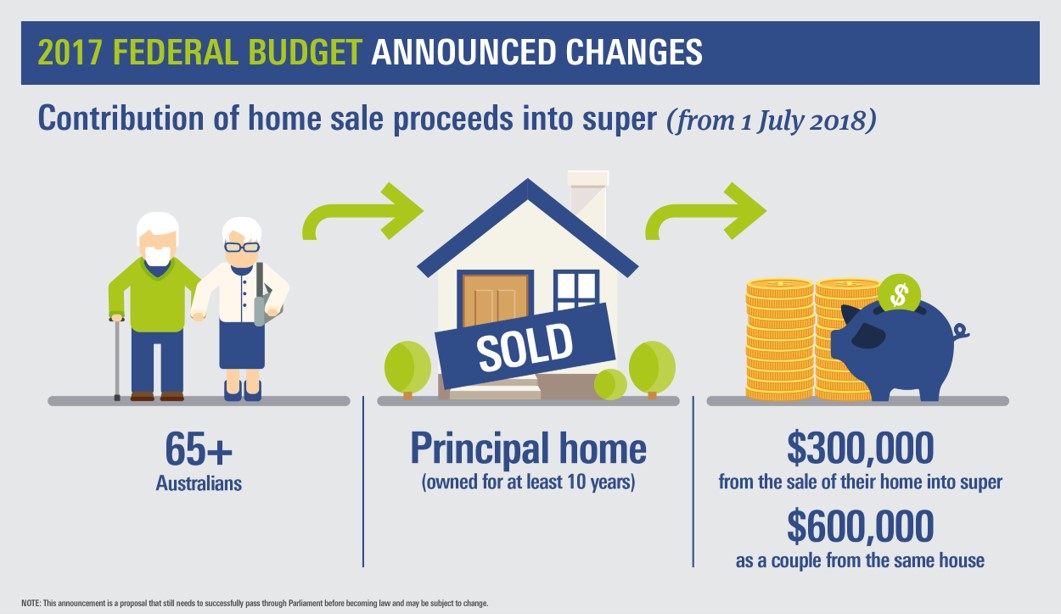

As you’re not doubt aware, the Federal Government announced it’s 2017 Budget this week and one of the surprise outcomes was the Downsizing Contribution for those looking to move out of a larger family home. Here’s a little more about how that works…

Downsizing contribution

People aged 65 or over will be able to make a non-concessional contribution to their superannuation of up to $300,000 each from the proceeds of selling their principal residence.

- Work test does not apply

- Residence must be held for a minimum of 10 years

- Total superannuation balance restrictions of $1,600,000 do not apply

- Restrictions eased on people aged 75 or over.

Downsizing contribution Case Study

John is 75 and Jane is 69 and they both have retirement income streams. They sell the home they have lived in for more than 10 years to downsize and the proceeds are $2,000,000.

George has room under the $1.6 million transfer balance cap. He can make a non-concessional contribution of $300,000 to superannuation and may choose to use the contributed proceeds to start a new account-based pension.

Jane has already used her transfer balance cap. She can make a non-concessional contribution of $300,000 to superannuation. As she has no room under her cap she cannot start a new pension with the contributed proceeds.

It’s worth having a chat with your Adviser to see if this is the best strategy for you, as you may lose Centrelink entitlements, depending on your new circumstances.

by Jodie | May 1, 2017 | Budget, Centrelink, Finances

The chances are you dutifully file your tax returns every year but are you making the most of your government entitlements? In this article,

we guide you through some key entitlements available for families.

Are you confused about your government entitlements? The good news is the recent overhaul of the Department of Human services no longer means lengthy waits in government office queues or listening to hold music while trying to organise your childcare rebate.

With automated payments and the user-friendly MyGov website, there has never been a better time to take a fresh look at your entitlements.

The birth of a child

Taking time out to care for a newborn can be expensive. However, since January 2011 primary carers now have access to government-funded parental leave payments, which are currently made for up to 18 weeks. There is also a 2-week payment available to eligible dads or partners assisting with a newborn.

Assistance with childcare

To encourage parents with young children to remain in the workforce, there are some great benefits on offer to working parents.

If you have children attending approved childcare and meet the income test (currently below $160,308 for families with two children), you may be entitled to the Child Care Benefit to help with the cost of daycare, vacation care or before and after-school care.

Higher income families may still claim the Child Care Rebate, which covers up to 50% of out “of pocket childcare expenses, up to an annual limit of $7,500.

Assistance for low to medium income families

Single parents and low to medium-income families can take advantage of a range of tax breaks and payments that can make raising a family more affordable. These include:

- The Single Income Family Supplement, which provides an annual payment of up to $300 to

help eligible households. The main income earner must earn between $68,000 and $150,000 and any secondary income earner below $18,000.

- The Parenting Payment for single parents with children under 8 or parents with partners with children under 6 who meet certain income tests.

- Family Tax Benefit for lower income families with dependent children under 20 (which includes grandparents assisting with childcare).

Summary

We have outlined just a few of the benefits that can help with the cost of raising a family.

To find out more about your entitlements, visit the Department of Human Services website.

by Jodie | Apr 18, 2017 | Budgeting, Debt Management, Finances, Insurance & Protection, Investments, Money, Retirement

From wills to long-term budgeting, there’s a lot to think about when making your retirement to-do list. Here’s some tips to make sure you’ve ticked all the boxes.

1. Check your will

Without a valid will, an administrator will be appointed to manage your estate, which may cause your family plenty of problems. To save them the stress, ask a solicitor to draw it up for you and make sure you and two witnesses sign it.

2. Plan your estate

Think of your estate plan as your family’s stress-free action plan that they can turn to for guidance when you pass away. It should cover all of your documents, contacts, debts, bills and assets so your family can easily figure out what to do with them.

3. Budget for the long haul

Australians are living longer than ever – which means your retirement savings also need to last longer. Create a long-term budget that will help you live the lifestyle you want – and don’t forget about healthcare costs. Then comes the most important part of a budget – sticking to it.

4. Invest in your future

From boosting your superannuation to investing in shares, understanding your investment options can make a huge difference to your retirement savings. When you start investing – and you should start early – make sure you have a mix of investments to spread your risk.

5. Be wary of scams

Investment scams are on the rise in Australia, with perpetrators directly targeting retirees to access their superannuation funds. Protect yourself by never giving out your financial details over the phone or by email. And be suspicious of anything that sounds too good to be true.

6. Start thinking about insurance

Many insurance policies expire at a certain age, leaving you without cover. And if yours comes from your superannuation fund, it could be eroding your savings. From age-based insurance policies to products that cover funeral expenses, you should seek professional financial advice to develop a plan that is appropriate for you as you enter retirement.

by Jodie | Apr 2, 2017 | Finances, Investments, Retirement, Savings, Superannuation, Wealth

The Government has legislated changes to the Age Pension rules from 1 January 2017, which it estimates will see 300,000 Australians lose all or part of their pension entitlements.1

If you are retired or about to retire, some careful planning now may put you in shape to access at least a part Age Pension. Here we outline some strategies to consider.

Building up the super of the younger member of a couple

If you are retired and have a spouse who has not reached Age Pension qualifying age, making contributions to your spouse’s super account may be beneficial. This is because super in the accumulation stage is not counted towards the Age Pension assets or income tests until the member reaches Age Pension qualifying age or begins an account-based pension.

Gifting

Gifting money (for example to a family member or charity) can help to reduce your assessable assets. The Government has set a limit of $10,000 per financial year for a single person or a couple, limited to a total of $30,000 over a five-year period. If you are planning to gift more than the allowable limits, check the rules here as penalties may apply.

Pre-paying a funeral plan

While it is not something that everyone would like to consider, pre-paying for a burial plot or funeral expenses can make good financial sense. As well as saving your family expense when you die, prepaid funeral plans and burial plots are not assessable assets for Age Pension purposes.

Using certain income streams

Certain annuities are assessed more leniently under the Age Pension rules than other investments, which may help you to achieve a higher level of Age Pension.

When purchasing a term annuity, you can select the proportion of capital (residual capital value) you would like returned to you at the end of the investment term. Annuities with a residual capital value of less than 100% are generally assessed favourably under the income and assets tests.

Speak to your adviser for more details as the rules differ depending on when an income stream was commenced, its term and your life expectancy.

Summary

If you are concerned about how the upcoming changes to the Age Pension rules will affect you, arrange a meeting with your financial planner who can help you to structure your income and assets to make the most of your entitlements.

Source:

1. http://www.superguide.com.au/how-super-works/300000-retired-australians-to-lose-some-or-all-age-pension-entitlements

by Jodie | Mar 16, 2017 | Advisers, Insurance & Protection, Retirement

You’re retired, the house is paid off and the children are self-sufficient, – it may be time to review your life insurance?

Policies expire

People take out life insurance while they are working to protect their dependants if they die prematurely.

Life insurance policies, including income protection, trauma, and total and permanent disability (TPD) insurance, generally expire when you reach a certain age, even if you are still working. So, let’s consider some of the insurance products you may have and see how long they generally last.

Insurance options

Term life insurance is a popular policy option. Beneficiaries receive a lump-sum payment if the policy holder dies or suffers a terminal illness and the usual expiry age is 99.

TPD insurance is paid in a lump sum if an accident or illness prevents the policyholder from earning an income. The usual expiry age for this type of insurance is 65.

Trauma insurance covers a major illness or injury, such as a stroke or car accident. It covers specific events and is paid out in a lump sum that can be used for any purpose, such as living or medical expenses. The usual expiry age for this type of insurance is 70.

Income protection insurance covers loss of income caused by accident or illness. Typically, these types of policies pay 75 per cent of the insured person’s income but there are many variations in their terms. The usual expiry age for this type of insurance is 70.

What about my super?

There are usually additional rules for policies held within a superannuation fund. Life insurance coverage through super usually ends at the age of 65.

When deciding whether to take out or continue your life insurance, you may wish to consider such things as any outstanding debts, including any mortgage repayments, as well as the needs of those you leave behind.

Nevertheless, each person’s circumstances are different and if you are unsure of what you need, talk to your financial adviser.