by Jodie | Sep 22, 2016 | Advisers, Finances, Insurance & Protection, Money

If your life insurance policy is in a drawer gathering dust, your family could be in for a nasty shock in the event of a claim. Here we outline some pitfalls to avoid when taking out cover.

1. Buying on price rather than cover

No-one wants to pay too much for cover but the purpose of buying life insurance is to ensure your family won’t be left to fend for themselves in the event of your death.

Cheap policies can be riddled with potential issues, so read the fine print and look into the capacity

of the insurer to pay, policy exclusions and dispute handling processes.

2. Not considering insurance outside super

Many people make the mistake of thinking that life insurance cover through super will be enough. Most super funds provide a default level of cover but this is often well below the level required.

In some cases, people could be caught unaware that their insurance cover had lapsed if and when they changed jobs and switched out of the fund. However, on the plus side, since the introduction

of Choice of Fund, it is easier to carry over and elect to use your own superannuation fund when going into a new job. An individual’s insurance cover within their super fund remains intact as long

as they remain a member of that fund.

When it comes to insurance within superannuation it’s also important to remember that premiums

are paid from what is effectively your retirement savings, which can impact your overall super balance on retirement and when you begin drawing down on your savings.

3. Failing to get proper advice

Life insurance policies are easy to obtain these days and it can be tempting to buy policies online

or from a teleprovider. However, policies that are quick and simple to obtain may be declined at claim time for reasons such as non-disclosure, exclusions or hidden clauses.

Sitting down with a qualified adviser means you can benefit from unbiased advice on a broad range of policies that can be tailored to your individual requirements. The adviser will also discuss issues you might not have thought of- for example will your insurance policy be owned by you, your spouse, both of you, your super fund or a trust or corporate entity?

4. Failing to review cover when circumstances change

There are certain key events in life when it is imperative to take a fresh look at your insurance coverage.

Have you married or divorced or has your spouse passed away since you last reviewed your policy? Have you become a parent or have your kids left home? Have there been any changes in your financial circumstances such as an increase in income, more debt or paying off a mortgage?

All these are factors to consider when determining the level of your cover.

Summary

No-one wants their families to be left high and dry in the event of their death. Taking the time

to consider your life insurance today may be your greatest gift to your loved ones tomorrow.

by Jodie | Sep 22, 2016 | Advisers, Women

Wealth Planning Partners are pleased to announce that their Director Amanda Cassar has been named a finalist in the Female Excellence in Advice Awards for 2016.

CEO of the Association of Financial Advisers (AFA) Brad Fox, said the ability of this Award to attract so many women of such high calibre is a great indication of the industry’s progress in generating positive change for the future.

“Female advisers play a vital role in our industry in providing Australians with better access and more choice over who they partner with on their financial journeys. As a result, the Australian advice industry continues to get better, enabling it to provide great advice to more Australians.”

The Award criteria include assessment of the candidates’ contributions to financial literacy in the community and/or campaigns targeted specifically at helping female clients take control of their financial lives.

TAL, who are long term sponsors of the Award, General Manager of Retail Distribution, Niall McConville said the Award continued to attract and showcase some of the extraordinary female talent in the industry.

The winner for the AFA Female Excellence in Advice Award will be announced at the AFA National Conference in Canberra from 5-7 October 2016.

We would like to wish Amanda and all the finalists the very best for the announcement of the award winner and note that it’s the clients who are the real winners when such passionate ladies are their to assist with their financial needs..

by Jodie | Aug 31, 2016 | Advisers, Finances, Money, Retirement, Wealth

Planning your finances early means you are better placed to enjoy what really matters in your retirement. Read this guide to find out how.

Entering retirement is a significant change – but that doesn’t mean it has to be stressful. By starting to plan early and following a few simple steps, you can help reduce your worries as you transition.

Consider what lifestyle you want. Do you want to travel, move, study? Go on a cruise then settle down in a retirement village? Or downsize your home and live comfortably?

On a psychological level there are other considerations. For example, how will you fill your time in retirement and will it keep you sufficiently engaged and or give your life a sense of purpose? Have you thought about giving back to the community in some way, or working and or consulting part time?

How much money you’ll need will depend on a clear picture of all of your goals – both financial and your overall wellbeing.

Once you’ve decided on your retirement goals, you need to consider whether you’ll have enough money to support them. It’s important to think long term. A man who is 65 years old today could live 19 more years; a woman 22 years more. But you may live even longer. You’ll need to know how much super you will have by the time you’d like to retire, when you’ll be able to access your super and whether you’ll be eligible for the Age Pension.

You can use many online tools to calculate how much you’re likely to save during your working life. A financial adviser may also provide you with a thorough evaluation tailored to your current assets and super fund.

After coming to grips with your finances and how much you’ll need to save to fund your desired lifestyle, you can work out the appropriate retirement plan.

You may want to start a transition to retirement pension, which allows you to keep working while accessing your super. By continuing to work after you reach your preservation age (between 56

and 60, depending on when you were born), you can boost your retirement savings as your employer will continue to make contributions to your super and it’ll be taxed at a lower rate.

With a transition to retirement pension you can either continue to work full time or reduce your working hours and supplement your income with withdrawals from your super – but there are restrictions on how much you can withdraw. Which option you choose will depend on your desired retirement lifestyle. In the recent Federal Budget, the Government proposed to change the tax treatment of transition to retirement pensions. It is important to understand how these proposed changes may impact you.

If you are able to work past pension age, there are government incentives you can take advantage of, such as the Work Bonus. Under the Bonus, the first $250 of your employment income isn’t assessed in the pension income test, increasing the amount you can earn.

If you would like to retire and access your super once you reach preservation age, there are several ways you can manage your finances. You may set up a retirement income stream. This means you can withdraw certain amounts from your super fund at intervals so you don’t spend your savings too quickly.

Another option is to withdraw your super in cash or transfer it to a non-super account. This may be an appealing way to immediately clear debts, invest in assets outside super and make any significant immediate purchases. However, it may also lower your future income and attract higher tax rates.

Retirees can take advantage of numerous entitlements such as travel concessions, discounted medicine and other benefits that holding a Pensioner Concession Card or Commonwealth Seniors Health Card provide. If you are eligible, the Age Pension will provide you with payments as a supplement to your savings.

Retirement can be an exciting time of transition. By organising your finances now you are better equipped to enter your retirement with far less stress, more purpose, and free to enjoy what’s ahead.

[1] Australian Bureau of Statistics, Life Tables, States, Territories and Australia (November 2014). Accessed from https://www.moneysmart.gov.au/media/332959/financial-decisions-at-retirement.pdf

by Jodie | Aug 22, 2016 | Debt Management, Finances, Insurance & Protection, Money, Wealth

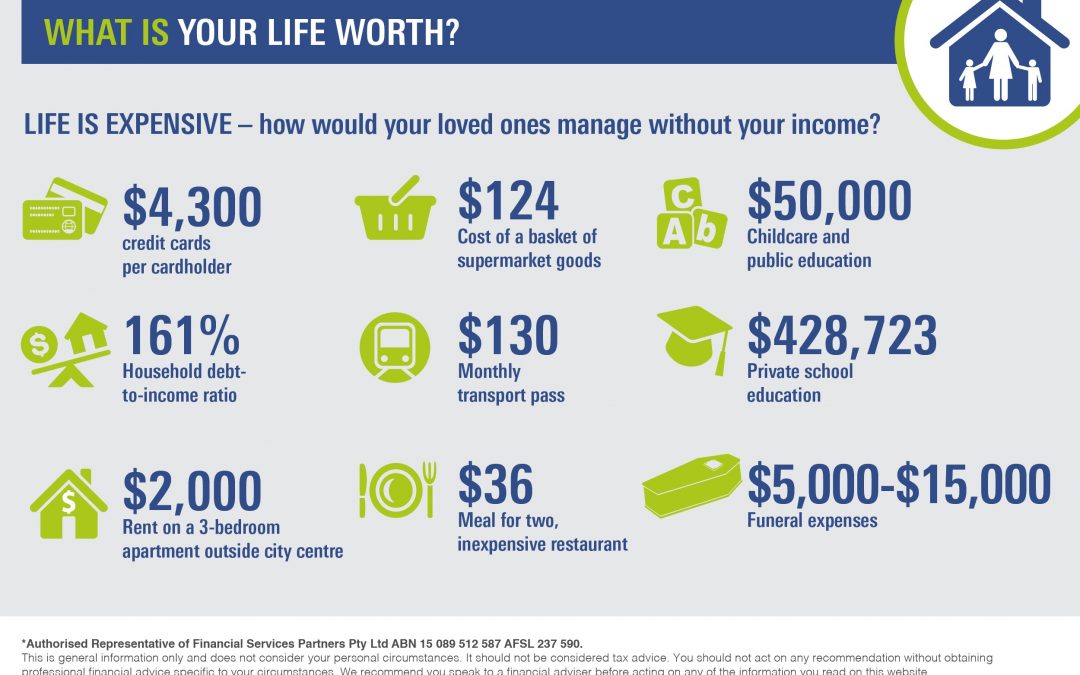

With the majority of Australians still dangerously underinsured, is it time you reviewed your cover?

Jeff is a clean-living 53-year-old who exercises regularly, doesn’t smoke, enjoys a healthy diet and only indulges his love of good wine at the weekend.

Yet things changed suddenly for Jeff last year when he awoke one night to find he couldn’t breathe. His wife called for an ambulance and he was rushed to hospital, where he was taken into life-saving surgery following a heart attack.

After waking from his operation, Jeff was in deep shock. While he knew there was a family history of heart disease, he had gone to great lengths to prevent the onset of the illness and had not properly thought through how his family would cope without him.

During his recovery, Jeff reviewed the life insurance component of his super and discovered that in the event of his death his family would receive just $300,000, which would barely pay off their mortgage. He had not taken into account daily living expenses, car loans, his daughters’ school fees, his wife’s low income or their inadequate savings.

Fortunately for Jeff his story is a positive one. Now in better health and back at work, he has spoken to a financial adviser and taken out additional life insurance, albeit at a significant premium following his heart attack. He and his adviser are also looking into critical illness cover, which would pay out a lump sum should he suffer another sudden illness.

In Australia, Jeff’s story is not uncommon. In fact, surveys have shown Australia has much lower levels of insurance than other developed nations including the US and UK1[1].

The required level of life insurance is now about $680,000, while the typical default cover is about $258,000 – a significant gap2[2].

Could your loved ones make ends meet if you were unable to work or died?

Here are some of the things you should consider:

- Mortgage or rent costs

- Daily living expenses – food, bills, transport

- Childcare

- School and university fees

- Other expenses – house repair costs, medical expenses

Please give us a call to make an appointment to discuss your insurance needs and ensure you are adequately covered.

[1] Lloyd’s Global Underinsurance Report 2016

[2] Rice Warner Underinsurance Research Report 2014

by Jodie | Aug 15, 2016 | Aged Care, Australian Economy, Budgeting, Centrelink, Finances, Money, Retirement

Choosing how you age is not just about accommodation for you or your family. There are also a range of financial and emotional issues to plan for.

The quality of today’s health care means we are enjoying longer lives, with current life expectancy levels far exceeding those of previous generations. Accordingly, many Australians ought to make well thought out plans for their living and care arrangements in their later years a top priority.

But, some research alarmingly tells another story.

The insights

# A 2011 survey on housing in later life revealed that one quarter of the 5000 baby boomer respondents hadn’t considered the issue of their financial futures with respect to aged care at all.[1]

# Over 31% of respondents said they expected to rely on the government for their future housing and financial needs as they age, highlighting a gap in overall awareness of the social security system.

# Prior to 1 July 2014 most aged care facilities utilised an accommodation bond for residential aged care* – only one in three respondents understood how bonds worked, highlighting a gap

in financial literacy. (*Since July 2014 this has been replaced with refundable accommodation deposits/contributions.)

# Importantly, the same study also highlighted that over 64% of people would prefer to age in their current homes, rather than downsizing or moving into aged care.

# More than 353,800 people in Australia have dementia and by 2030 the number will grow to more than 500,000 according to peak body Alzheimer’s Australia, underscoring the importance

of planning for aged care early.[2]

The demographic shift

Currently, there are 400,000 Australians over the age of 85; approximately 1.2% of the population.2 However, the overall proportion of the population is expected to almost double to 5% by 2050 according to the Australian Bureau of Statistics.[3] Recent research from Calibre Consulting Engineers, tips that this seismic shift will stretch infrastructure considerably. The group predicts $22.5 billion worth of new aged care facilities will be required before 2031 to house this ageing population, especially as more baby boomers enter retirement.3 Also, for every 1000 people over the age of 70, 88 will need government assistance to afford aged care.[4]

The private vs public sector

Some pundits expect the private sector to step up to accommodate the gap in demand and supply. The ASX-listed aged care provider Estia, which has recently been the subject of media attention, has for example publicly slated plans to expand its number of beds from 4639 to 10,000 by 2020 as reported in The Weekend Australian recently.[5]

However, private sector growth on this magnitude could potentially be affected by recent cuts in government funding, which included a proposed $1.2 billion cut to the aged-care sector in the Liberal Party’s Federal Budget released in May.

Calibre’s Civil and Urban sector leader Brent Thomas is concerned that signs of further cutbacks and lack of political support will mean “prices will rise for available sites, and many seniors will be unable to afford the type of care they need in areas they want to live”.[1]

Aged care fees – have you factored them in?

Based on the current trend of cutbacks to this sector, the costs of aged care may well increase in the future. If that occurs it could also place significant stress on all of us as and when we age,

as well as our families. It’s important to therefore understand some of the main costs involved. For those considering residential aged care solutions there are two predominant costs.

Entry costs: also known as ‘accommodation payments’ are means-tested and can be paid as a lump sum, daily amount or a combination of both.

Ongoing costs: may include a basic daily fee, capped at 85 per cent of the single person basic Age Pension, a means-tested care fee and additional services fees.6 Costs for home care recipients include a basic daily fee that can be up to 17.5 per cent of the single person basic Age Pension.[2]

What can a holistic financial plan include?

With changes in government funding, plus the possibility of rising costs of living and higher housing prices, a holistic financial plan for later life is vital. Such plans can include:

- Timing or advice on aged care: i.e. funding options before the need to rely on aged care.

- Power of Attorney/guardianship: i.e. to help enable lifestyle, financial and medical decisions

in the event of reduced capacity.

- Choice of accommodation, understanding fees and accommodation payments/contributions

for aged care facilities and the implications of selling or renting the family home

- Tax planning

- Estate Planning

- Social security entitlements

- Cash flow/Budgeting and debt planning

- Home improvements: i.e. modifications to your existing family home such as installing ramps; rails; single levels; electrical controls; bathroom and kitchen safety features and accessibility-planned homes.

Emotional concerns and the importance of objective advice

Other facets of aged care strategies are the emotional concerns of both people facing this stage of life, as well as their families. It is vital that plans and conversations are documented and had well ahead of any declines in health and or mental cognisance. These often difficult conversations can

be significantly aided by an independent and objective third party, such as a financial adviser. Underscoring the importance of this step is the rising number of people expected to suffer from dementia in Australia by 2030, from more than 353,800 people currently, to more than half a million by 2030 according to Dementia Australia.[3]

Acceptance of moving to aged care can be particularly difficult and emotionally fraught, highlighting the case for a documented plan. According to the AHURI survey, considerations including access to familiar areas, family and friends are cited as vital aspects to include in a plan, which may or may not involve selling the family home.[1]

The flood of information available can also be hard to navigate. This is where a trusted financial adviser can play an important part of planning for the future and providing objective advice to assist you and your family.

COMMON QUESTIONS

What is “the means test” for residential aged care?

This examines your assessable income, including your Age Pension, as well as your assets, including your superannuation and in some circumstances, the value of your home.

What impact can it have on my aged care fees?

The result of this test will determine the costs you’ll be required to pay if and when you enter aged care accommodation and any ongoing means tested care fees.

Can I get in-home care still?

Yes, but when you are applying for home assistance an income test will determine how much you will pay; people with a higher income and or with a larger asset base will generally pay more.

Where to from here?

It’s essential to act early and make sure you have a plan in place; whether that is to stay in your existing home and seek in-home care, or to enter an aged care facility. By planning ahead and saving early you can establish your preferences as to how you age and put in place steps to maintain your financial wellbeing.

[1] Bridge, Davy, Judd, Flatau, Morris, Phibbs. (2011, September) ‘Age-specific housing and care for low to moderate income older people’ Report No. 174 for the Australian Housing and Urban Research Institute, UNSW-UWS Research Centre.

[2] ‘Greens Funding for Better Dementia Care Welcomed’, (2016, 22 June) Alzheimer’s Australia, Press Release, sourced at: https://fightdementia.org.au/media-releases/greens-funding-for-dementia-care

[3] Watkins, J. (2016, June 16). We need to speak up for our parents. The Sydney Morning Herald. Retrieved from http://www.smh.com.au/comment/we-need-to-speak-up-for-the-aged-20160615-gpjfag.html

[4] Australian Bureau of Statistics, 2015

[5] Cranston, M. (2016, June 1). $22.5 billion in Aged Care homes needed but will it be achieved? The Australian Financial Review. Retrieved from http://www.afr.com/real-estate/225-billion-in-aged-care-homes-needed-but-will-it-be-achieved-20160530-gp7qhr

[6] Ibid.

[7] White, A. Loussikian, K. (2016, June 11). Aged care and fast money an unhealthy mix. The Australian. Retrieved from http://www.theaustralian.com.au/business/aged-care-and-fast-money-an-unhealthy-mix/news-story/e56d693e174eb8e935834aec50ff6c6b

[8] Money Smart. Aged Care. Retrieved from https://www.moneysmart.gov.au/life-events-and-you/over-55s/aged-care

[9] ‘Greens Funding for Better Dementia Care Welcomed’, (2016, 22 June) Alzheimer’s Australia, Press Release, sourced at: https://fightdementia.org.au/media-releases/greens-funding-for-dementia-care

10 Ibid.

11 Bridge, Davy, Judd, Flatau, Morris, Phibbs. (2011, September) ‘Age-specific housing and care for low to moderate income older people’ Report No. 174 for the Australian Housing and Urban Research Institute, UNSW-UWS Research Centre.