by Jodie | May 12, 2017 | Australian Economy, Finances, Taxation

Budget 2017 has proposed a few tax changes. Read about them here:

Medicare levy

- Rises from 2.0% to 2.5% from 1 July 2019 to help fund the National Disability Insurance Scheme.

Capital gains tax discount for investors in affordable housing

- Managed investment trusts will be allowed to develop and own affordable housing. Investors will get a capital gains tax discount of 60 per cent.

- Investors will get a capital gains tax discount of 60 per cent provided that they invest in qualifying affordable housing.

Small business accelerated depreciation extended

- Immediate deduction of assets up to $20,000 extended to 30 June 2018.

Education costs

- Eligibility for student payments will be limited to people undertaking courses approved for VET student loans.

- Existing student payment recipients will be grandfathered for the duration of their current course unless there is a break in their payment entitlement.

- You may wish to consider this if you want to fund your child’s education costs.

by Jodie | May 12, 2017 | Finances, Investments, Money, Wealth

The Government has announced some Incentives to improve housing options. Among these, are:

- Allowing first-home buyers to save a deposit through voluntary contributions to superannuation

- Disallowing travel deductions for investment residential property

- Limiting depreciation deductions for plant and equipment on residential investment properties

- Tightening the capital gains tax rules for foreign investors

- Reforming foreign investment rules to discourage investors from leaving properties vacant.

First-home buyers can use super

- First-home buyers will be able to use voluntary contributions to their existing superannuationfunds to save for a house deposit.

- Contributions and earnings will be taxed at 15 per cent, rather than marginal rates, and withdrawals will be taxed at their marginal rate, less 30 basis points. Contributions will be limited to $30,000 per person in total and $15,000 per year.

- Both members of a couple can take advantage of the scheme.

- Non-concessional contributions can also be made but will not benefit from the tax concessions apart from earnings being taxed at 15%.

First-home deposit salary sacrifice case study

Louise earns $60,000 a year and wants to buy her first home. She directs $10,000 of pre-tax income into her superannuation account using salary sacrifice, increasing her balance by $8,500 after the contributions tax has been paid by her fund. After three years, she is able to withdraw $27,380 of contributions and the deemed earnings.

After withdrawal tax, she has $25,760 she can use for her deposit. Louise has saved about $6,240 more for a deposit than if she had saved in a standard deposit account. Louise’s partner, Craig, makes the same income and salary sacrifices $10,000 over the same period. Together, after three years, they have $51,520 for their first home, $12,480 more than if they had saved in a standard deposit account. (Source: 2017 Budget papers)

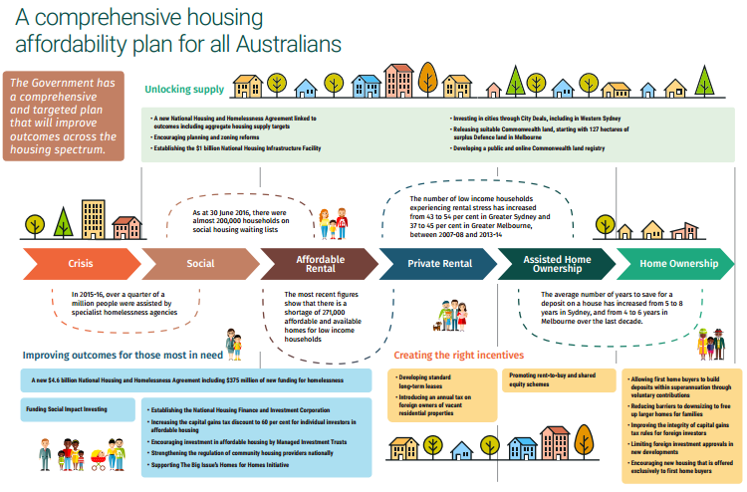

Unlocking supply

- The Government will help boost housing supply by:

- Providing $1 billion facility for critical infrastructure, such as water supplies

- Working with the States on planning and zoning reform to speed up development

- Releasing suitable Commonwealth land, starting with Defence land at Maribyrnong in Melbourne

- Investing more than $70 billion from 2013 to 2021 on transport infrastructure

- Specifying housing supply targets in new agreements with the States and Territories.

by Jodie | May 11, 2017 | Australian Economy, Centrelink, Finances, Money

Lots of Social Security changes have been proposed in Budget 2017. Here’s a highlights list of some of these. Please note that these are not yet enshrined in law.

Reinstating the Pensioner Concession Card

- This will be reinstated for pensioners who lost their pension following changes to the pension asset test on 1 January 2017.

- Those granted the Commonwealth Seniors Health Card (CSHC) as a result of the

- January changes will maintain entitlement to this card (and the energy supplement).

- The Low Income Health Care Card issued as a result of the January changes will be deactivated.

One-off energy assistance payment

- $75 for single and $125 per couple for qualifying pensions on 20 June 2017.

Family Tax Benefit Part A

- Changes to the income test for the Family Tax Benefit Part A payments may reduce entitlements. We need to identify and manage the impact of these changes.

Liquid assets waiting period

- The maximum waiting period for payments will increase from 13 weeks to 26 weeks and apply

where liquid assets are equal to or above $18,000 for singles (formerly $11,500) without

dependants or $36,000 (formerly $23,000) for couples and singles with dependants.

- It’s important to seek advice early (before termination) to see if we can lessen the impact of these changes. If you are affected, we need to manage cash flow during this period.

Newstart eligibility

Activity tests other than voluntary work may be required to receive Newstart allowances for people aged between 55 and 59.

Former Farm Household Allowance

Recipients who do not receive any other Commonwealth income support will be eligible for loans of up to 50% to refinance their debt to a maximum of $1 million.

Residency test changes

To be eligible for the Age Pension or Disability Support Pension, some claimants will need 15 years of continuous Australian residence (up from 10 years). Generally this won’t affect existing recipients.

Consolidation of payments

- Seven working-age payments and allowances, including NewStart, will be consolidated into one payment called a JobSeeker payment.

- Key elements include aligning the participation requirements for recipients aged 30 to 49 with those for recipients under 30, and recipients aged 55 to 59 will only be able to meet up to half of their participation requirements through volunteering.

- Recipients aged between 60 and Age Pension age will have a new activity requirement of 10 hours per fortnight that can be met through volunteering.

by Jodie | May 11, 2017 | Australian Economy, Budget, Money, Taxation

WINNERS!!

First home-buyers

First home-buyers can save for a deposit by salary sacrificing into their super.

Downsizers

Downsizers, 65+, can contribute up to $300,000 each to super from the sale the family home

regardless of satisfaction of the work test, total super balance or if aged 75 or over.

Investors

Negative gearing stays for mum and dad investors but travel claims for investment residential properties will be denied and capital expenditure eligibility will be tightened.

Schools

$18.6 billion has been earmarked for extra funding for schools over the next decade.

LOSERS!!

Taxpayers

The Medicare levy will increase to 2.5% to help fund the National Disability Insurance Scheme.

Tertiary students

University fees will rise by $2,000 to $3,600 for a four-year course and students will have to start paying back their debt when they earn more than $42,000 from July next year, down from $55,000. A 2.5 per cent efficiency dividend will be applied to universities for the next two years.

Child care changes

Only to families with incomes below $350,000 per annum (in 2017-18 terms) will get the child-care subsidy from 2 July 2018. The upper threshold will be indexed annually from 1 July 2018.

Banks

The five biggest banks will be charged a levy, raising $6.2 billion over four years.

Tax avoiders

The ATO will target tax avoidance by multinationals and big business.

by Jodie | May 11, 2017 | Advisers, Australian Economy, Budget, Finances, Retirement, Superannuation

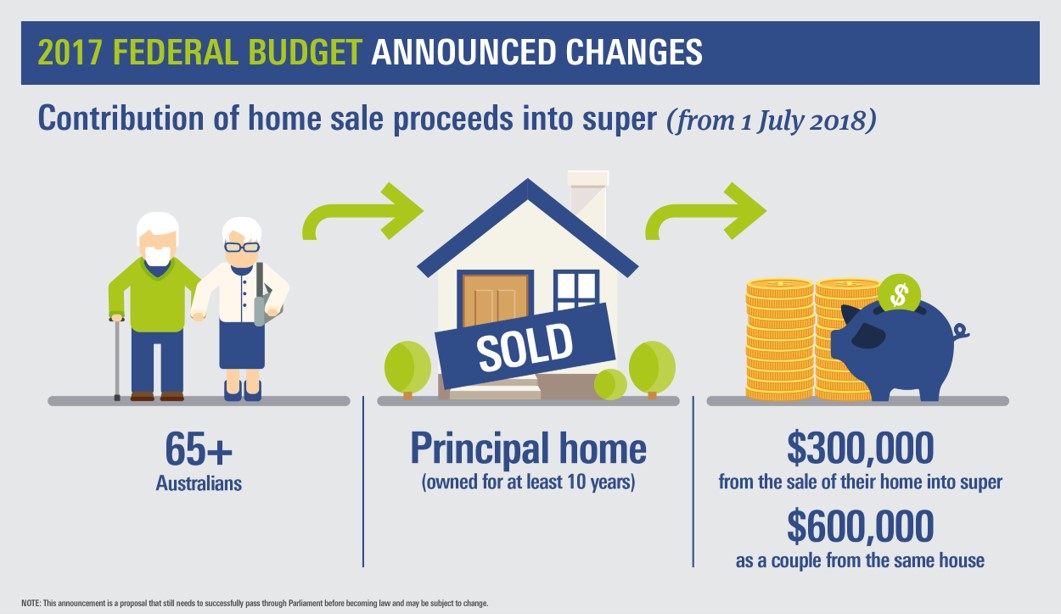

As you’re not doubt aware, the Federal Government announced it’s 2017 Budget this week and one of the surprise outcomes was the Downsizing Contribution for those looking to move out of a larger family home. Here’s a little more about how that works…

Downsizing contribution

People aged 65 or over will be able to make a non-concessional contribution to their superannuation of up to $300,000 each from the proceeds of selling their principal residence.

- Work test does not apply

- Residence must be held for a minimum of 10 years

- Total superannuation balance restrictions of $1,600,000 do not apply

- Restrictions eased on people aged 75 or over.

Downsizing contribution Case Study

John is 75 and Jane is 69 and they both have retirement income streams. They sell the home they have lived in for more than 10 years to downsize and the proceeds are $2,000,000.

George has room under the $1.6 million transfer balance cap. He can make a non-concessional contribution of $300,000 to superannuation and may choose to use the contributed proceeds to start a new account-based pension.

Jane has already used her transfer balance cap. She can make a non-concessional contribution of $300,000 to superannuation. As she has no room under her cap she cannot start a new pension with the contributed proceeds.

It’s worth having a chat with your Adviser to see if this is the best strategy for you, as you may lose Centrelink entitlements, depending on your new circumstances.