by Amanda Cassar | Oct 12, 2020 | Finances, General, Insurance & Protection, Money

Get ready for storm season!

The Queensland Government want everyone to Get Ready for disaster season. Use the 3 Step “Get Ready” Plan.

Prepare your household this storm season by completing these 3 simple steps:

- Have a plan Firstly, ensure your family is equipped with an emergency and evacuation plan. Make sure everyone knows what to do in a disaster. Team-up with your neighbours for added assistance if required. The Queensland government have put together a Household Emergency and Evacuation Plan form.

- Pack Supplies Secondly, have an emergency kit ready to go. A stocked “Go Bag” will ensure you are ready for storm season. This provides easy access to essential items that will equip your household for at least 3 days of isolation. Your kit should be in a sturdy waterproof

storage container. Make sure it is stored in a safe, easily accessible place within your home. And, ensure it is childproof if necessary. Be sure to let everyone know the kit’s location and document it in your emergency plan.

storage container. Make sure it is stored in a safe, easily accessible place within your home. And, ensure it is childproof if necessary. Be sure to let everyone know the kit’s location and document it in your emergency plan.

Please click here for a list of what to include.

- Make sure you’re covered Finally, the importance of having home and contents insurance cover is paramount. Many have found out too late that they did not have adequate insurance cover. Queensland has been impacted by over 70 significant natural disasters since 2011!

And, Step 3 is to make sure your insurance is enough to cover the costs of rebuilding your home and or replacing your possessions. For instance, both home owners and renters should check policies to ensure they are fully aware of what is covered.

What to ask your Insurer…

So, in conclusion, some questions to ask your insurance provider are:

- What disasters does the policy cover?

- How do they define each disaster?

- How much will the policy cover?

- Does the policy provide enough insurance to cover the cost of rebuilding your house and any extra costs you might incur?

- Is your insurance adequate to cover the replacement of your possessions?

- Are your possessions covered for damage caused by potential local hazards, such as storm, cyclone, flood and bushfire?

- In what circumstances will the insurer reject the claim?

- Are you covered for the cost of temporary accommodation if your home is uninhabitable?

- Does pre-existing damage caused by a previous natural disaster or lack of home maintenance impact eligibility of insurance claim payouts?

For how to Get Ready for Storm Season, visit the Qld Government website.

As a result, you’ll be ready to go in the event of any disasters. Or get in touch with the Team at Wealth Planning Partners, your Gold Coast Advisers to find out more. And ask, what do you need to do to Get Ready for Storm Season? Don’t leave it too late.

by Amanda Cassar | Oct 7, 2020 | Australian Economy, Budget

Federal Budget Update 2020 is out. See how this may affect your family.

Proposals

The Federal Budget Update 2020 is out, and is all about jobs, and spending to make more jobs. We already have JobSeeker and JobKeeper, and now we have JobMaker and JobTrainer.

The announcements in this update are proposals unless stated otherwise. These proposals need to successfully pass through Parliament before becoming law and may be subject to change during this process.

Announcements…

Each announcement the Treasurer made was translated into jobs. Tax cuts for 11 million taxpayers equals 50,000 new jobs; expanding the instant asset write-off and the carry back of current losses is another 50,000 jobs. Bringing forward the Stage 2 personal income tax cuts were the order of the day, and there will be no increases in tax in order to pay for spending. So unlike other economic downturns, there will be no deficits tax on high income earners.

One key theme throughout the Budget, is that the Government is keen to improve outcomes for young people. We know this recession has hit young people hard and many have taken early release of their super.

For more information about how the Budget may affect your family, click here.

Or contact your Gold Coast advisers at Wealth Planning Partners to see if you’re impacted. Call your Financial Planners at Robina on 07 5593 0855 to discuss further.

by Amanda Cassar | Sep 28, 2020 | Advisers, Australian Economy, Budget, Budgeting, Finances, General, Retirement, Superannuation

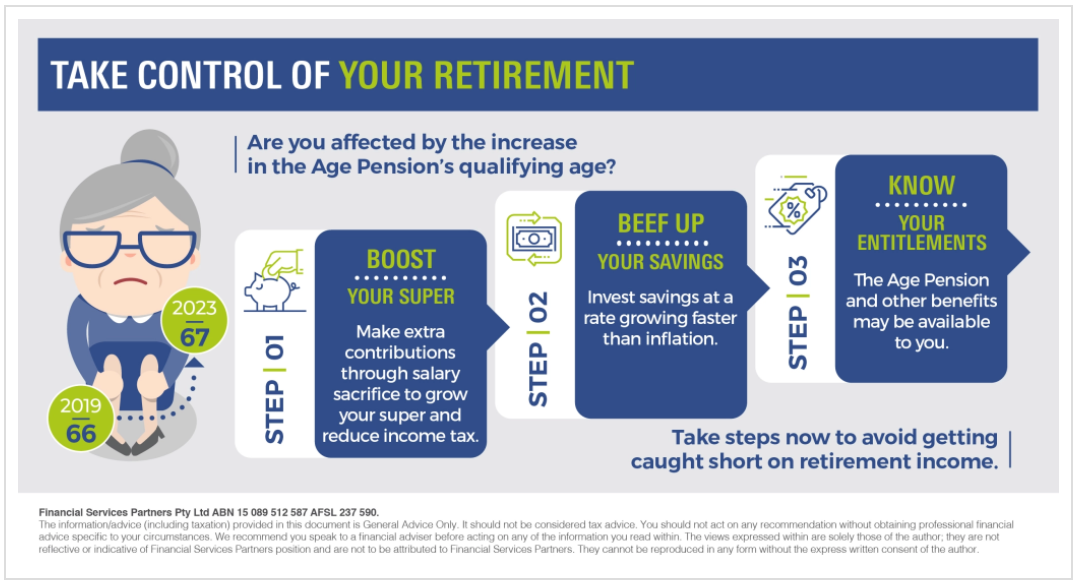

Are you affected by the increase in the Age Pension’s qualifying age? Take steps now to avoid getting caught short on retirement income.

The minimum age to qualify for the Age Pension has started going up. For those born on or after 1 July 1952, the qualifying age increases by six months every two years until it reaches 67 in July 2023. It rises to 66 in July this year.

So, if you’re turning 45 this year and plan to retire when you reach 60, you will need to wait until 67 before you can apply for the Age Pension. You’ll have to rely on your own savings and super. This makes it crucial to ensure you have enough money put away. But, the good news is that there’s still time to grow your retirement savings. So just how do you take control of your retirement savings?

Boost your super

Contributing more to your super can be a reliable route to bolstering your retirement fund. By making extra contributions through salary sacrifice, you can grow your super and at the same time reduce the amount of income tax you pay. The government will tax salary sacrificed contributions at 15 per cent. This could be much lower than your personal marginal tax rate.

Making non-concessional or after-tax contributions is another option. You can contribute up to $100,000 each financial year if your total superannuation balance is less than $1.6 million. To understand how these contributions work, it’s wise to get professional advice.

Jump onto the MoneySmart Superannuation Calculator to see how much you could have in retirement.

Beef up your savings

Your personal savings can supplement your super payments in retirement. But are they growing enough now to provide you with some income when you retire?

To build up your savings, you may have to invest part of it and make sure it’s growing faster than the rate of inflation. Investing in a managed fund or buying an investment bond may help you increase your nest egg. Seek professional advice to see if these instruments are appropriate for you.

Know your entitlements

Besides the Age Pension, you may be eligible for other government benefits and concessions. The Seniors Card, offers individuals over 60 discounts on some commercial and public services. Concessions that allow you to buy prescription medicine at a discount are also available.

But keep in mind that these benefits have strict eligibility rules. There’s also no guarantee that these entitlements will still be available by the time you retire. So take charge of your retirement today. By working with your financial adviser, you can develop a strategy that helps ensure you’ll be well provided for regardless of changes to pension policies.

If you’d like more information on how to take control of your retirement savings, reach out to the Team at Wealth Planning Partners.

by Amanda Cassar | Sep 28, 2020 | Advisers, Finances, Investments, Money, Savings, Self Managed Superannuation Funds, Superannuation

So, how do you invest your money? When deciding how to go about investing those hard earned dollars, you need to decide whether you’ll:

- do it yourself, or

- pay a financial advisor to do it for you

Both options have their pros and cons. However, you can – of course, do a bit of both.

Buy, sell or invest yourself

The advantage of choosing to invest yourself is that you’re in control of all the decisions. It will also save you money by making it cheaper than paying a financial advisor to invest your money. The down-side risk is that you may overrate your expertise and may not diversify.

If you choose to invest directly, it’s important to have a thorough plan and put in the time to research your investments. You should also keep track of how they’re performing.

Use a professional investment manager

If you decide to invest in a managed fund, some managed accounts, exchange-traded fund (ETF) or a listed investment company (LIC) your money is pooled with other investors. A professional investment manager then buys and sells investments on your behalf.

When using a professional, you benefit from their skills and expertise to make investment decisions. However, have to pay fees for this service. These can include management fees, administration fees and entry and exit fees.

See managed funds and ETFs to learn more about these investments.

Investing with a financial adviser

Seeking a financial adviser can assist you further by setting your financial goals, understand your risk tolerance and find the right investments that are suitable to you and your circumstances.

Make sure your financial adviser has an Australian financial services (AFS) licence or is an authorised representative. Check their qualifications on the Financial Advisers Register.

- Decide what it is that you want from the advice. Would you like help with investing money, budgeting or planning for retirement?

- Ensure that you read your adviser’s Financial Services Guide (FSG) to learn about their fees and services, and how they deal with complaints.

- Do your due diligence by comparing the fees charged by different advisers, to make sure you’re getting a good deal.

- Be careful about how much access your adviser has to your investment accounts.

Ensure that you talk to your adviser if you have any questions with regards to their advice and ensure that you understand their explanations in full.

If you’d like the Team at Wealth Planning Partners to assist, we’d be more than happy to help. Just reach out on 07 5593 0855.

by Amanda Cassar | Sep 21, 2020 | Advisers, Budgeting, Economy, Finances, Financial Stress, Investments, Retirement, Savings, Superannuation

Is it time to consider your retirement lifestyle needs?

Considering the cost of living and your expected annual retirement income, is crucial to retirement planning.

So, how do you consider your retirement needs? For the record number of Australians transitioning into retirement, the increasing cost of housing is a hindrance. Many are struggling to pay off their property before they retire, and this may lead to a few common scenarios:

- Being forced to sell the family home prior to retirement and renting or downsizing

- Continuing to pay down the mortgage on the home they live in, but leave beneficiaries with an asset that has debt owing

- Long-term renting due to lack of affordable properties on the market

- Short-term renting in different locations as a way of chasing the nomadic lifestyle dream without the financial burden of a mortgage.

And. deciding where and how you want to live can be fraught with stress. This can occur whether you’re about to retire or you’re if you’re watching your parents prepare for retirement. A recent survey by National Seniors Australia outlined that many people worry they will run out of savings and investments in retirement. Women worry more about retirement savings than men. Worrying is 65% higher in people who have less than $500,000 in savings. And at least 53% higher in people who expect their main source of income in retirement to be the Age Pension.[1]

How much money do you need to retire comfortably in Australia?

According to the Association of Superannuation Funds of Australia (ASFA), there are two broad categories of lifestyles in retirement — comfortable or modest. A comfortable retirement affords people a good car, private health insurance, dining out regularly, travel, and factors enjoyed whilst working. In a modest retirement, you may be entitled to the Age Pension, but you can only afford the basics, with occasional small luxuries.

How much do you need to live on?

There are facts and figures from industry bodies and experts, but your retirement lifestyle is unique to you. Mapping your retirement plan with a financial adviser can give you a clearer picture on what you can afford. As a benchmark, here are some widely touted figures:

- A couple of about 65 years of age – $40,194pa is needed to live modestly.

- A couple of about 65 years of age – $61,786pa is needed to live comfortably.

- For singles of about 65 years of age – $27,913pa is needed to live modestly.

- For singles of about 65 years of age – $43,787pa I needed to live comfortably.[2]

Can renting affect retirement income?

While these numbers help you understand cost of living in retirement, things become complicated if you don’t own your home. ASFA’s calculations are based on the assumption retirees will own their home before retiring. So, you don’t need need to allocate money towards mortgage or rent in the budget.

However, the Australian Bureau of Statistics (ABS) report that around 285,000 Australian households ren in retirement. While renting may afford the ability to live in a more desirable location, the cost still needs to be factored in. Therefore, the numbers provided by ASFA need to be tweaked if you are renting in retirement. And, this can blow out the figures of exactly what annual income you need to have access to.

Can you rent and afford a comfortable retirement?

Based on the ASFA’s calculations, if you retire in Sydney you would need $1,166,000 as a couple or $1,045,000 as a single. This is to afford a comfortable retirement lifestyle whilst renting. While the number may be lower for other cities and regional centres, it provides a more realistic calculation. Time to reassess exactly how much your retirement nest egg should be if you’ll be renting in retirement? Having a greater understanding of how you can structure your super funds can help you be better prepared.

As with other passive investments, ensure you’re not drawing down so much capital that your balance isn’t compounding. You need an adequate rate to provide you with enough retirement income for the rest of your life.

For example, if the average return on your super balance is 9% per year, it’s wise to drawdown 4% or less so you can maintain adequate funds. Retirement may be longer than you think? A good financial adviser can work through the calculations based on your individual circumstances, factoring home ownership or rent and any Centrelink benefits. Have you considered the retirement lifestyle you want without running out of money?

What if you don’t want to rent in retirement?

If you don’t own a home and you’re not keen on renting, there are other options. Maybe you want the freedom of living in a motor home, setting up in a modern tiny home, basing yourself in a retirement village, securing granny flat rights, or, living on a cruise ship. While these options may not be for everyone, the very nature of retirement, can give you the flexibility to live a nomadic lifestyle with a smaller carbon footprint. If you’re interested in staying in one place, a retirement village or granny flat can provide you with that lifestyle.

There is no one size fits all in retirement

When it comes to your retirement dreams and finances, your picture looks different to the next person. So, have you considered your retirement needs? If you don’t own your home, you’ll need to factor the cost of rent into your retirement planning. Be sure to ensure your nest egg and the annual income you’ll draw is enough to provide your desired retirement lifestyle. If you do own your home you won’t have to worry about the mortgage or rent. But, what about home improvements and modifications as you age?

With so many different scenarios to consider, it is wise to work through your options with your financial adviser. Reach out to the Gold Coast team of Financial Planners at Wealth Planning Partners if you’d like to discuss your individual needs.